Stochastic Process course note.

1. stochastic process

1.1. classes of process

Def: stochastic process

Note:

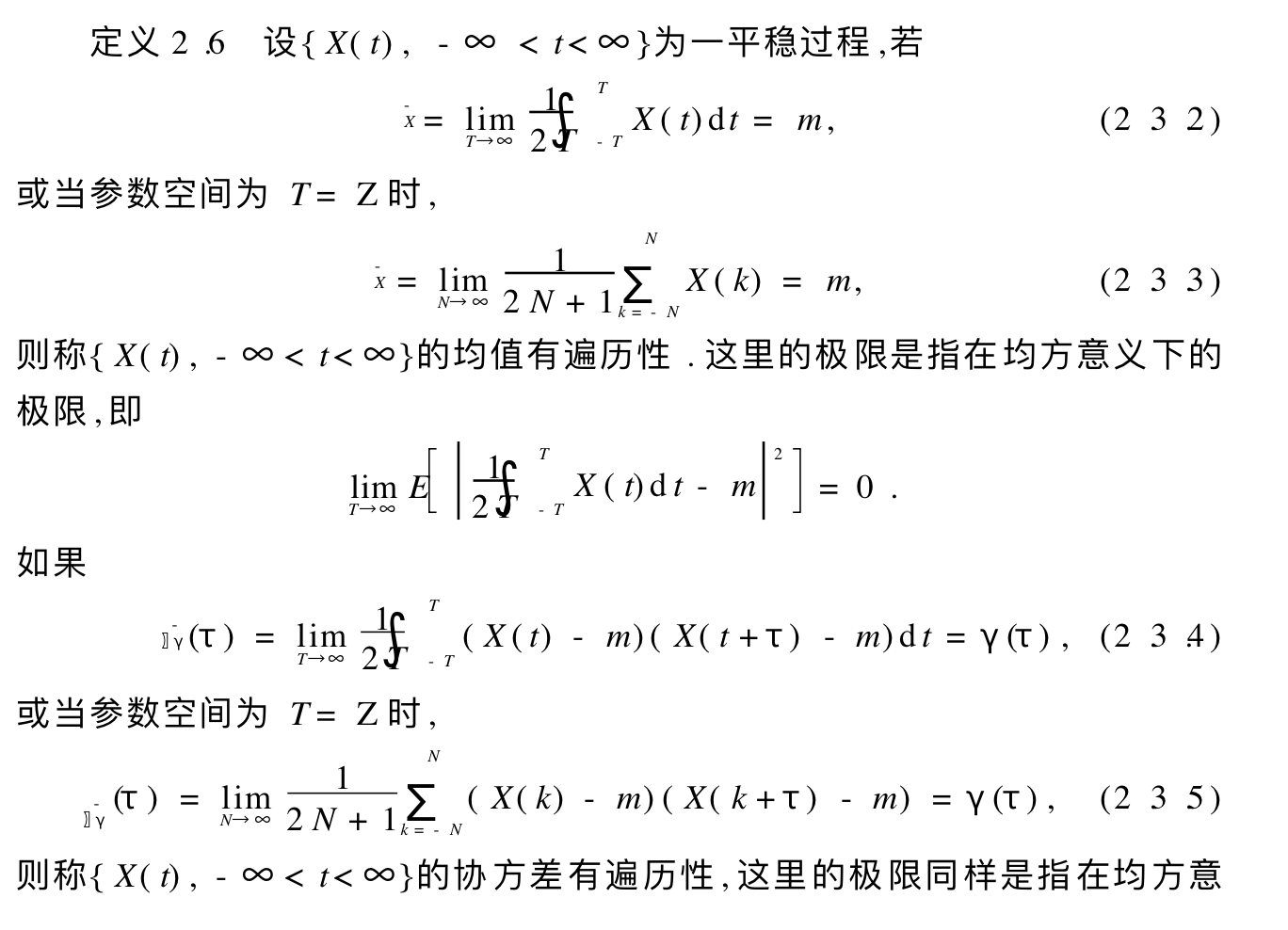

1.1.1. stationary

Def: stationary process

Note:

Def: broad stationary process

Note:

1.1.2. ergodic

Intro:

Def: ergodic process

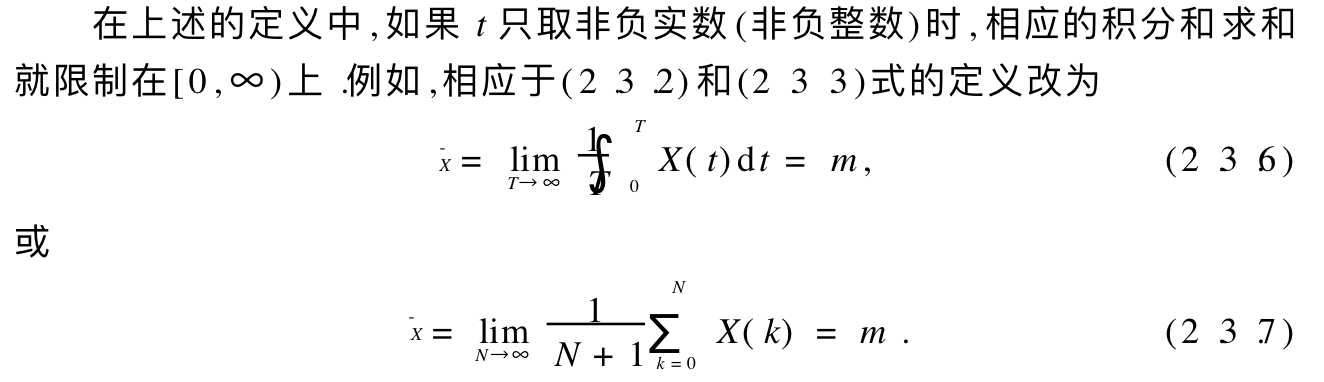

Note:

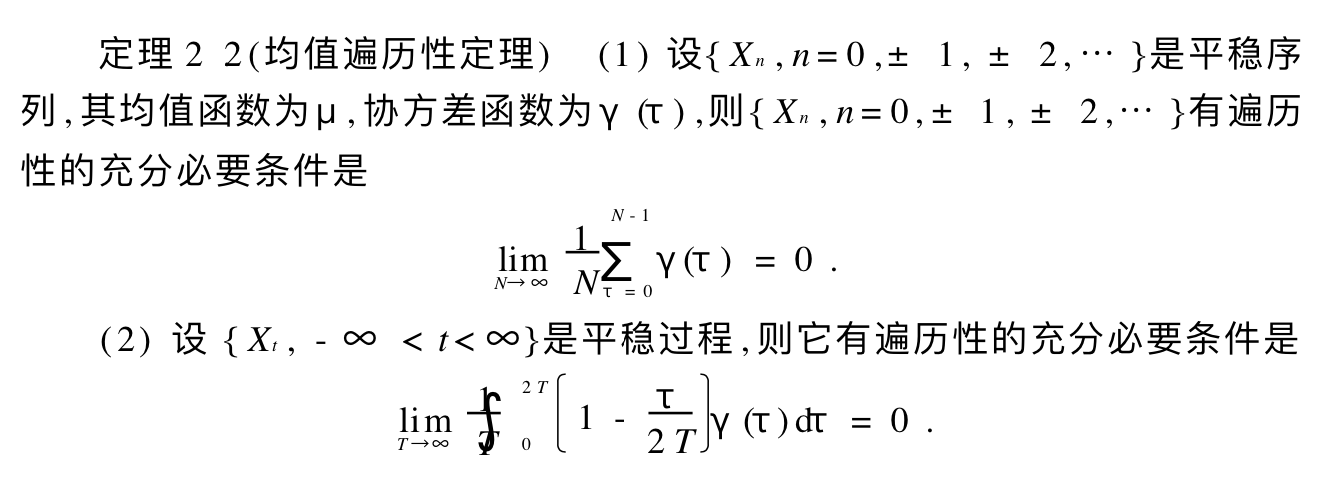

Qua: necc & suff

Qua: equation =>

Qua: equation =>

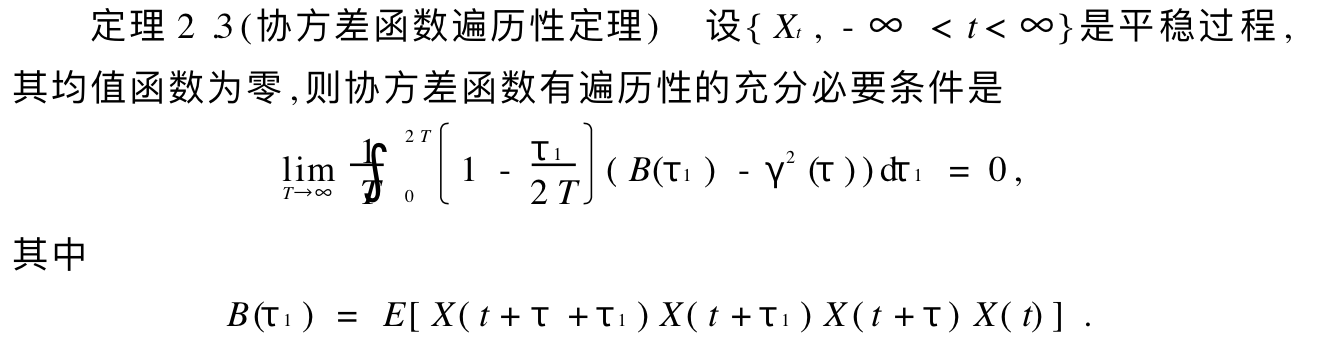

Qua: necc &suff for variance function

1.1.3. independent increment

Def:independent increment process

Note:

1.1.4. markov

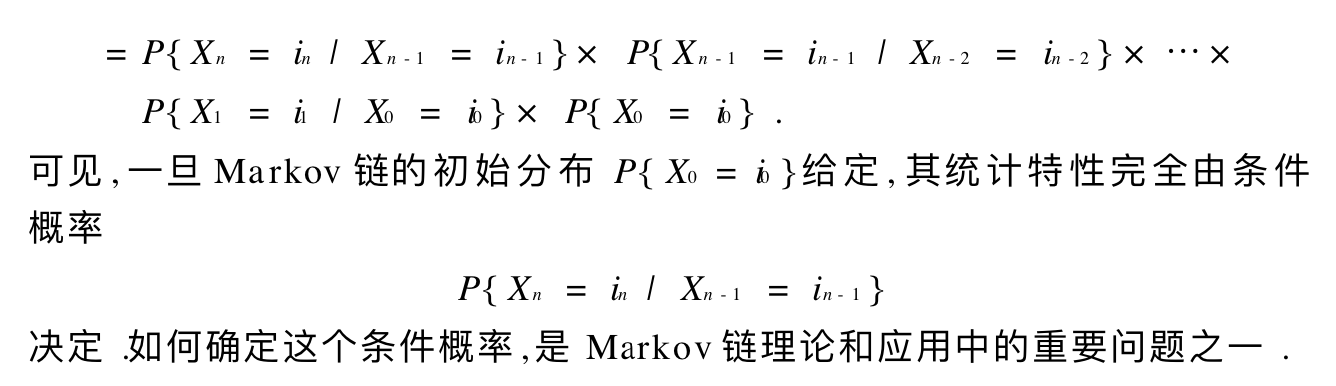

Def: markov

Note:

Note:

Note:

1.1.4.1. inhomogeneous markov

Def: inhomogeneous markov

Def: trans prob \(p _{ij}\)

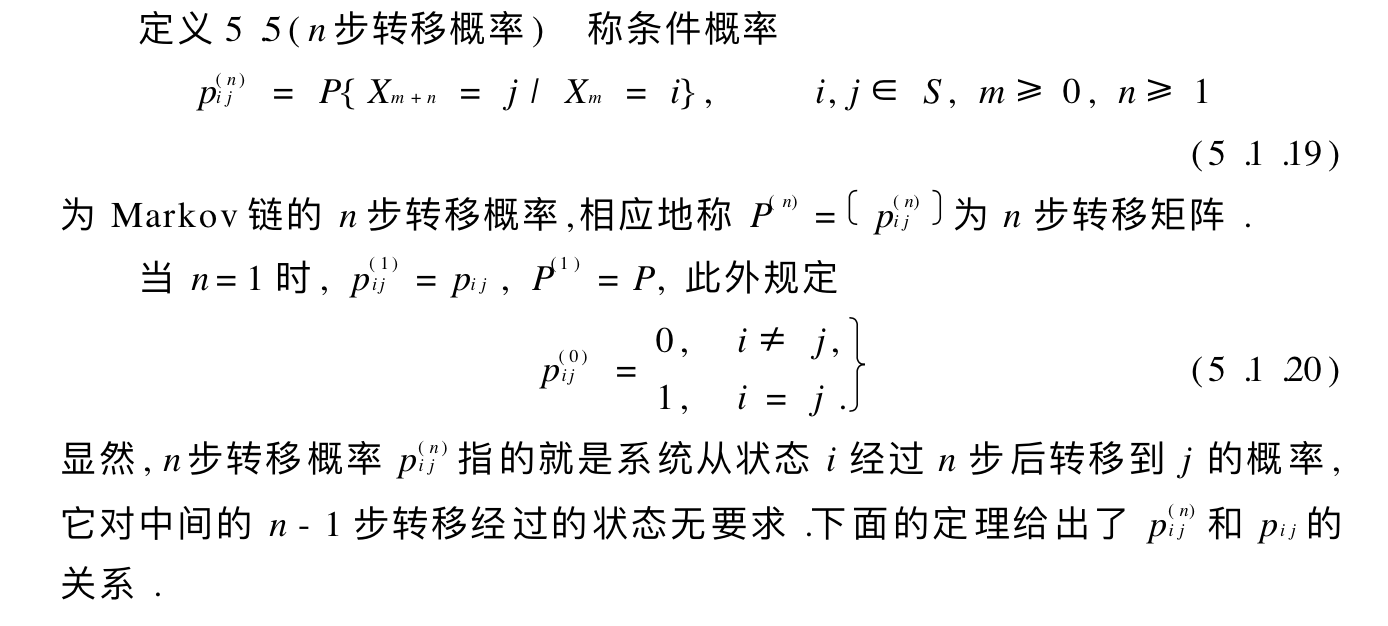

Def: n trans prob \(p_{ij}^{n}\)

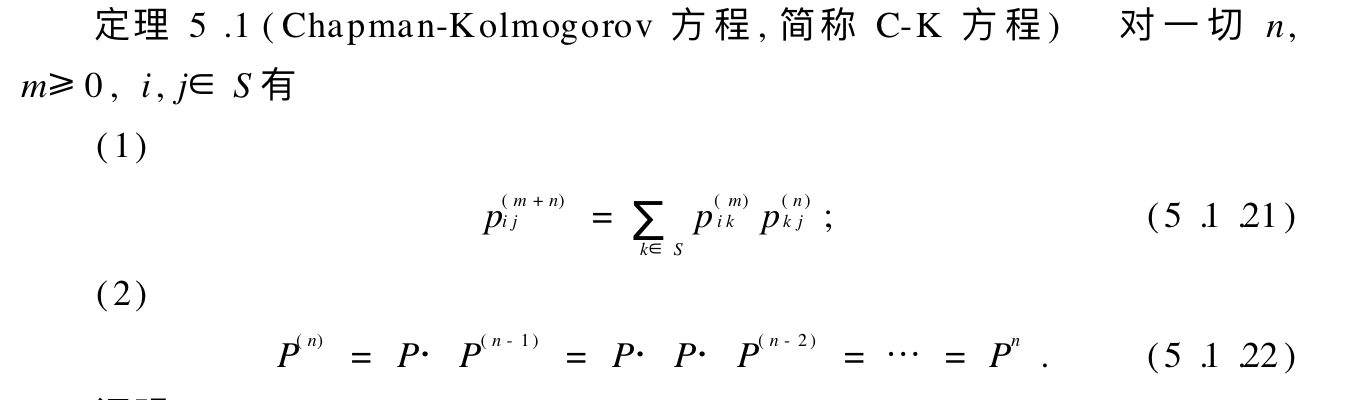

Theorem: relationship with pij

Theorem: relationship with fij

Def: prob matrix

1.1.4.2. reducible markov

Def: reducible markov

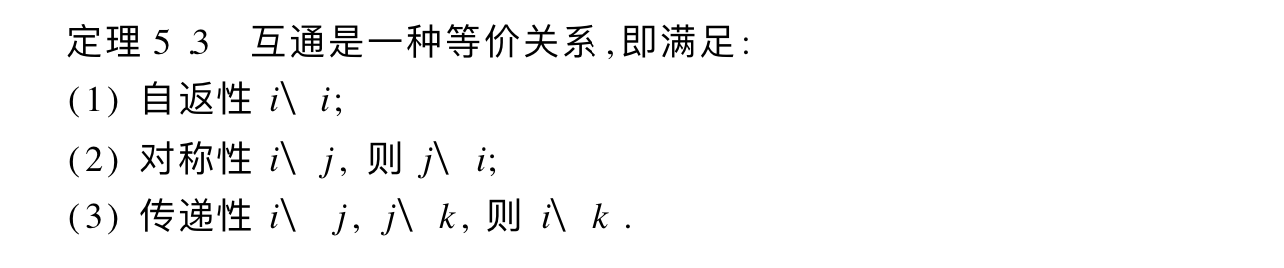

Def: property of status: same class

Note:

Qua: necc & suff

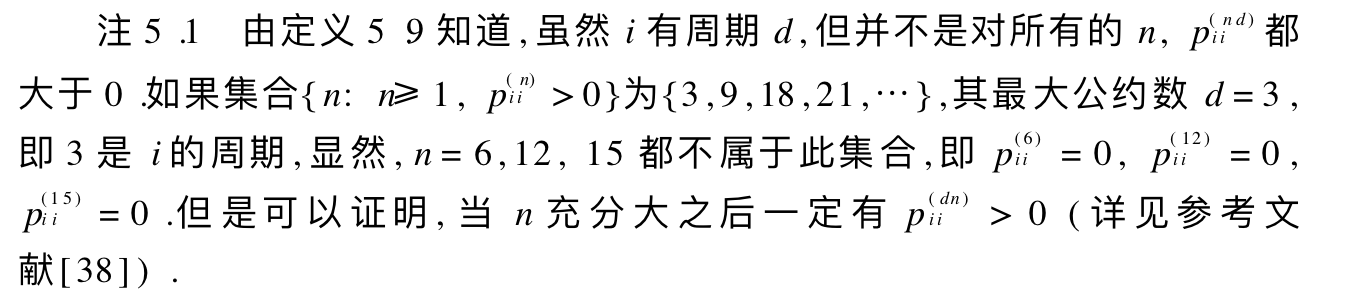

Def: property of status: circular

Note:

Qua: same status=>

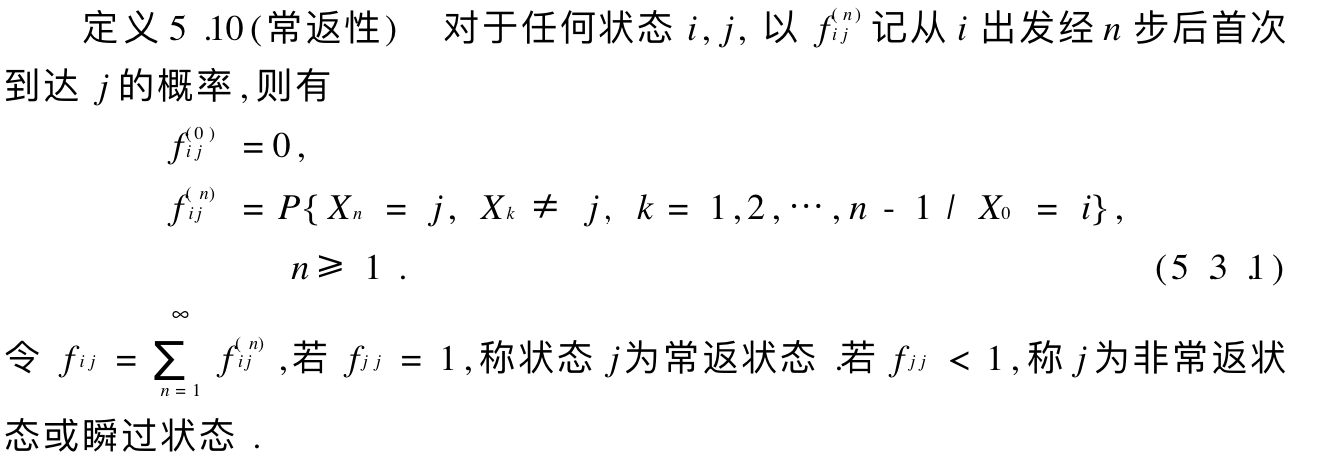

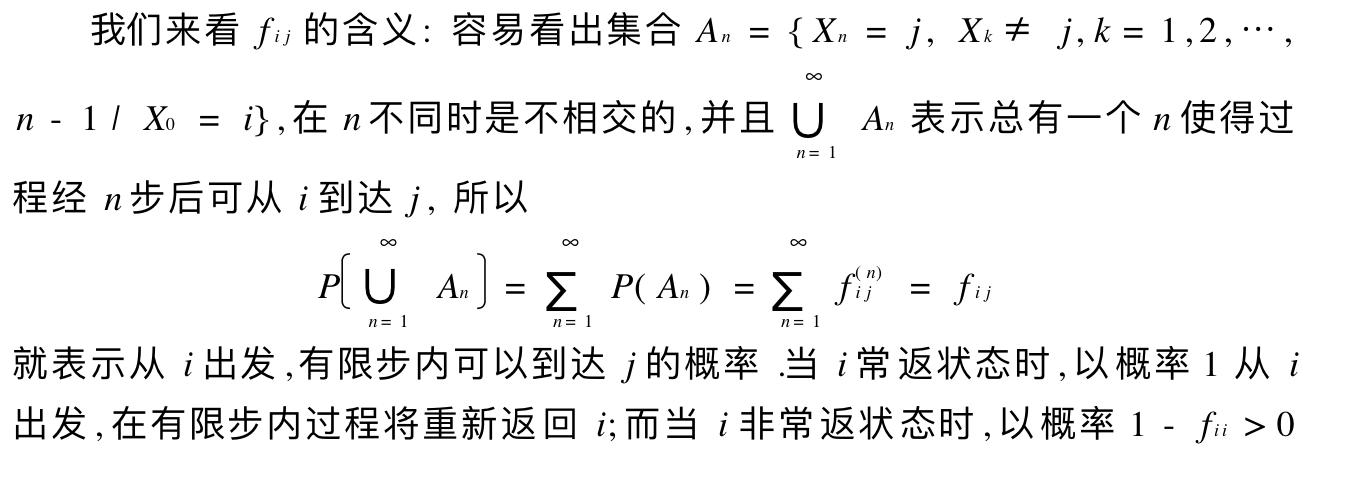

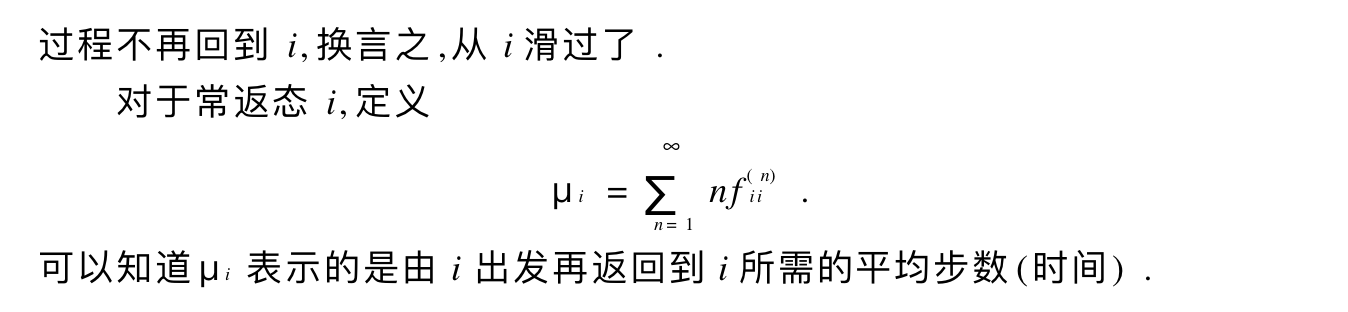

Def: property of status: Recurrence

Note:

Def:

Qua: necc & suff

Qua; => fji

Qua:

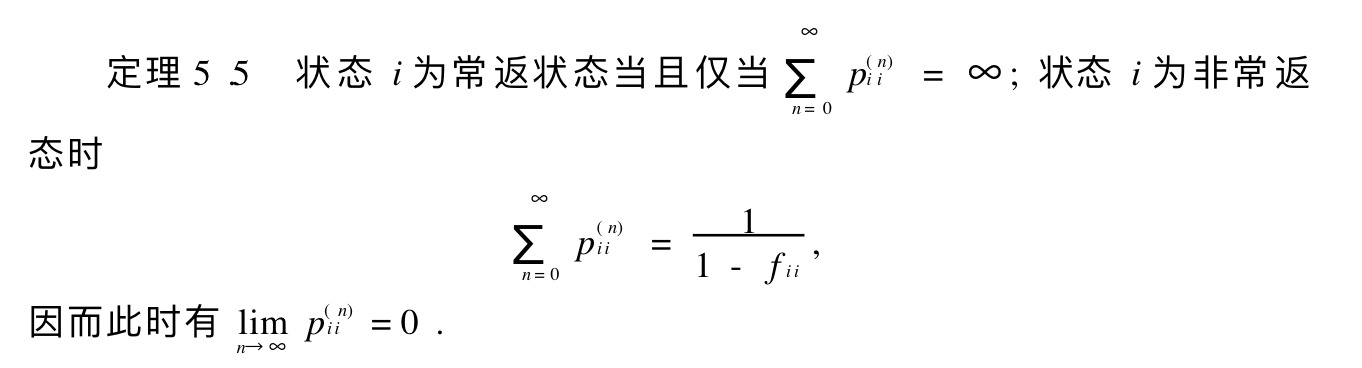

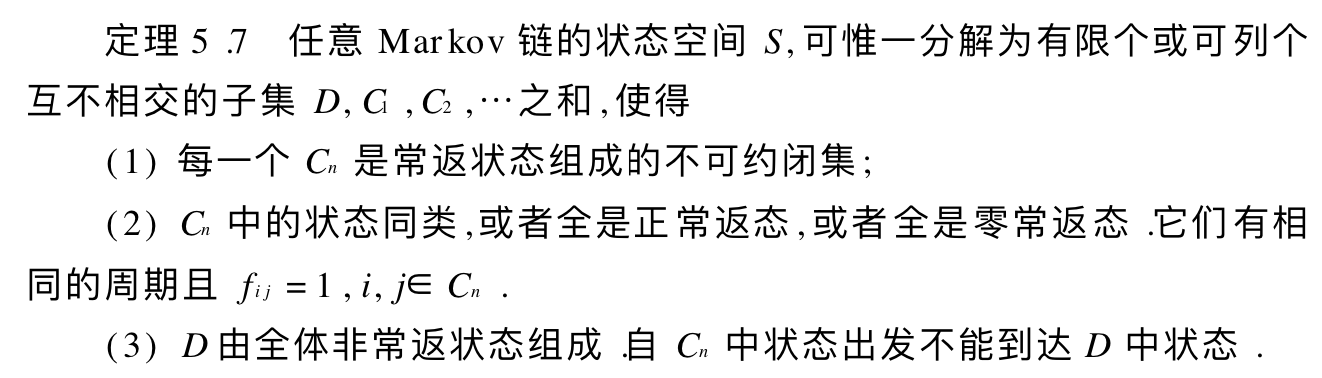

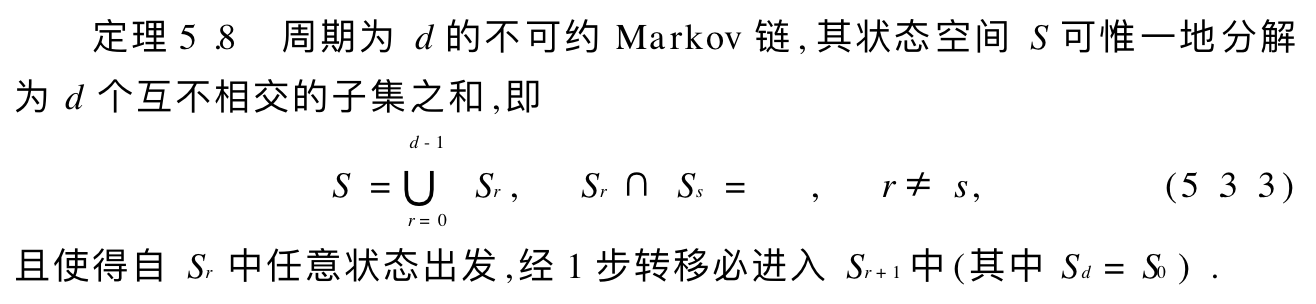

Theorem: =>decomposition

Theorem: => decomposition 2

1.1.4.3. limit markov

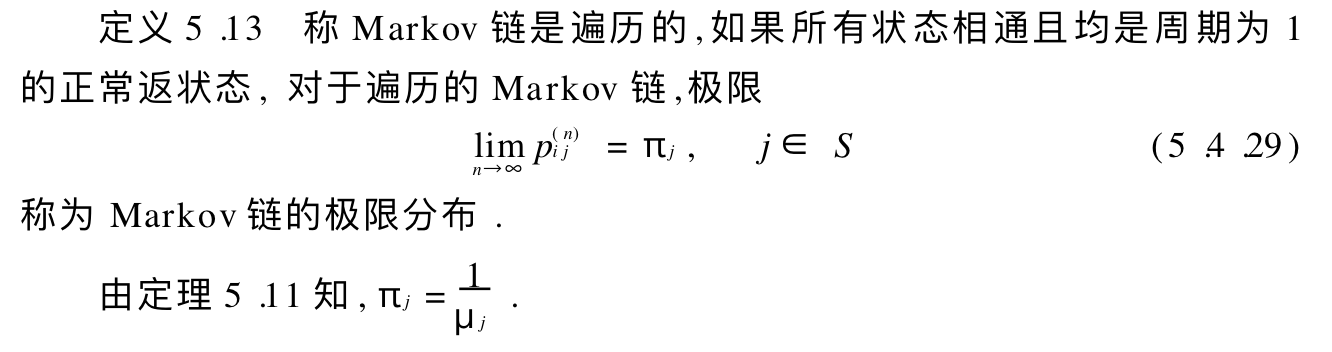

Def: limit markov

Theorem:

Note:

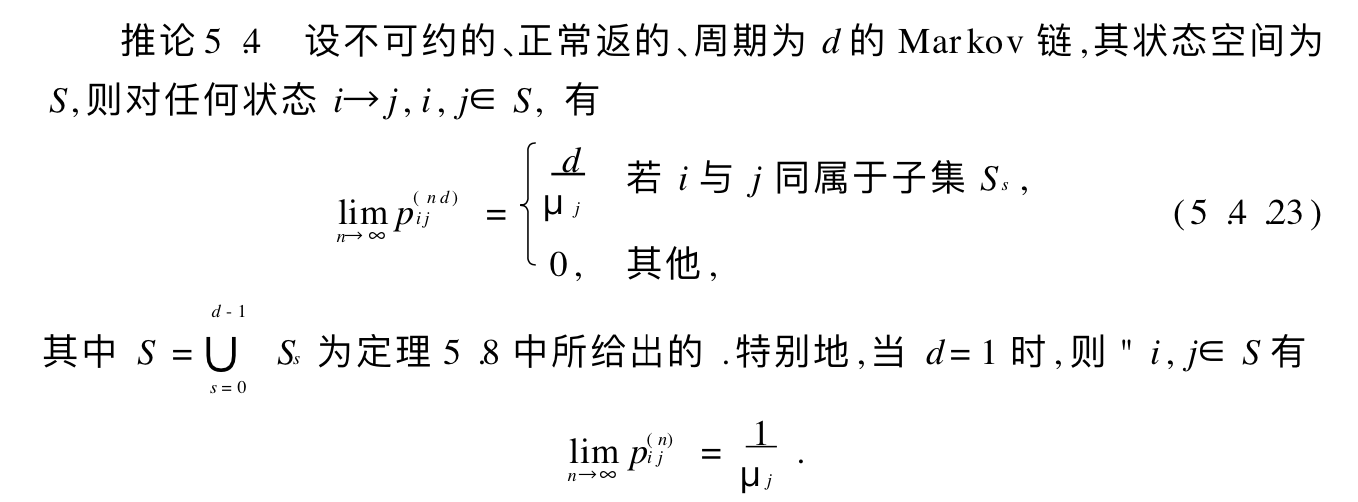

Corollary:

Theorem:

Corollary:

Corollary:

Theorem:

Corollary:

Lemma:

Theorem:

Corollary:

Note;

1.1.4.4. unchanged markov

Def: unchanged markov

Theorem: => relationship

Def: large number p109

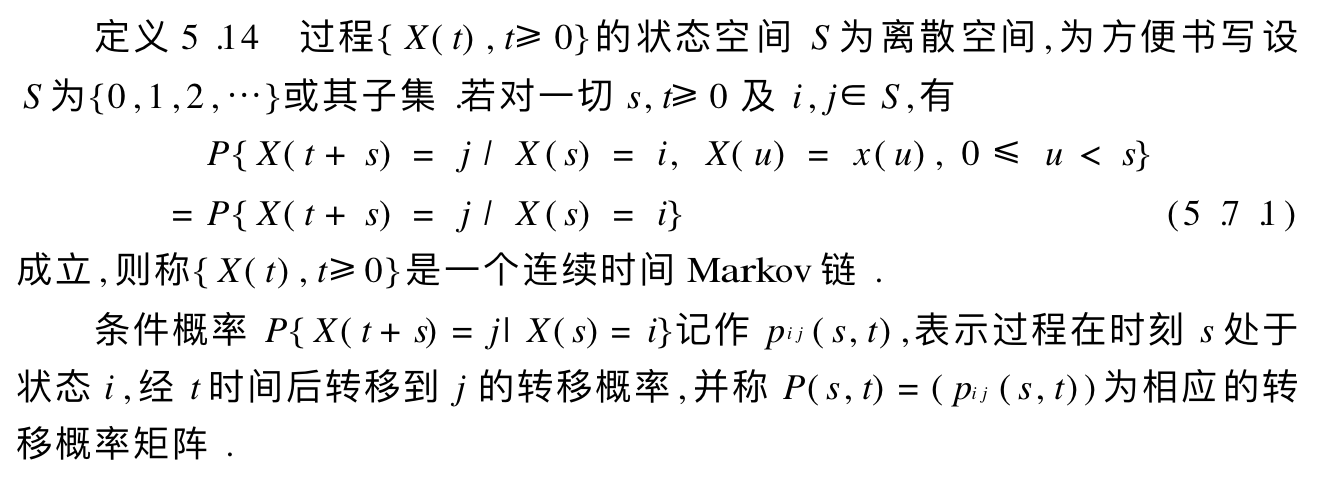

1.1.4.5. continuous markov

Def: continuous markov

Note:

Qua: => distribution

Note:

Def: regularized markov

Theorem:

Theorem:

Theorem:

Corollary:

Note:

Theorem:

Def: the final

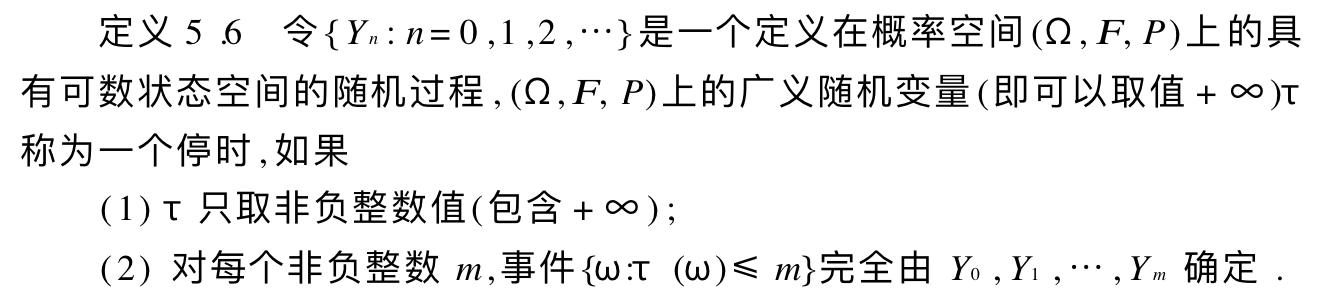

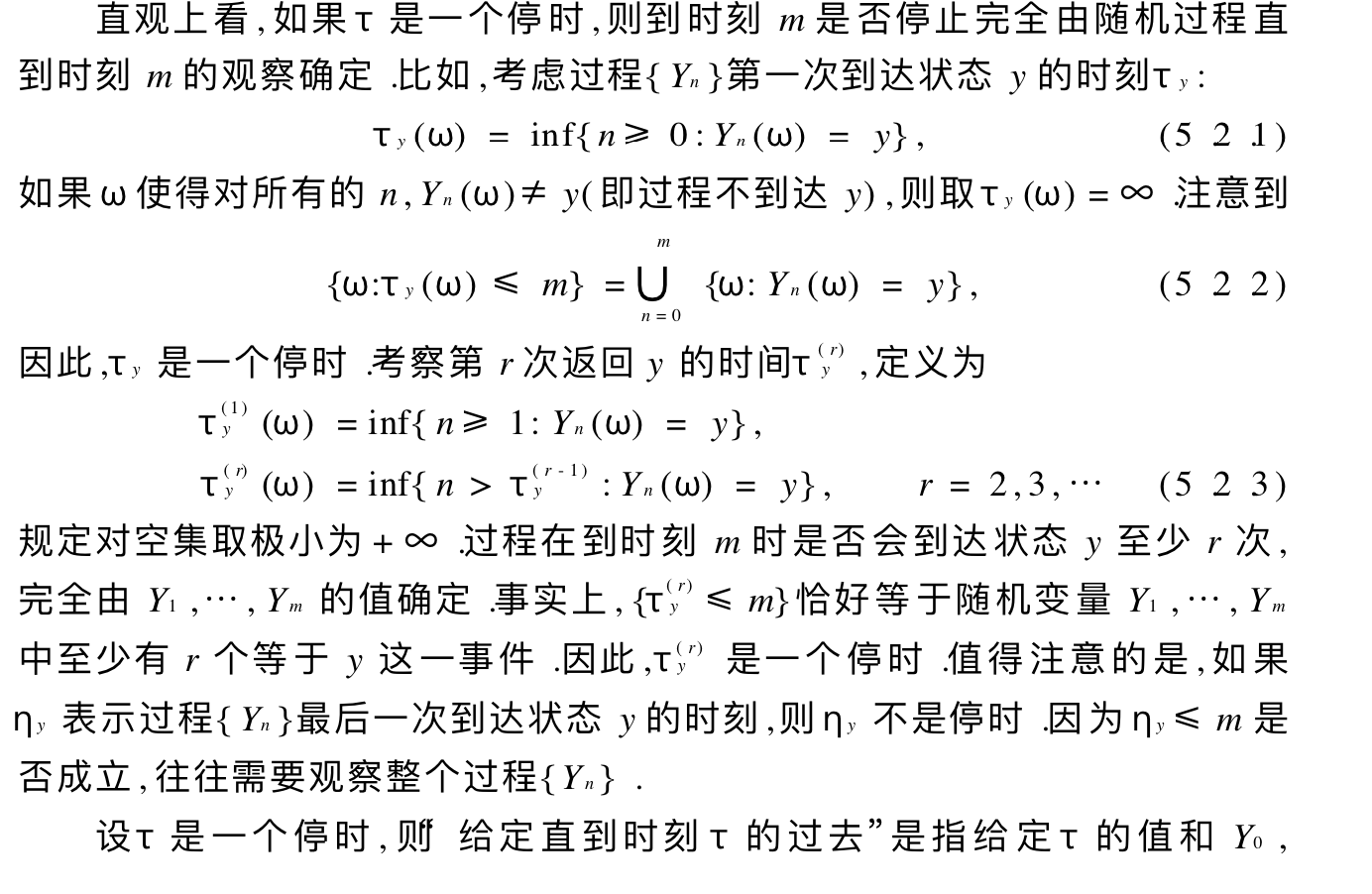

1.1.4.6. strong markov

Def: time stop

Note:

Def: strong markov

1.1.4.7. examples: population

1.1.5. Levy

Def

Def:

Def:

Def;

Def:

Def:

Def;

Def:

Theorem:

1.2. distribution

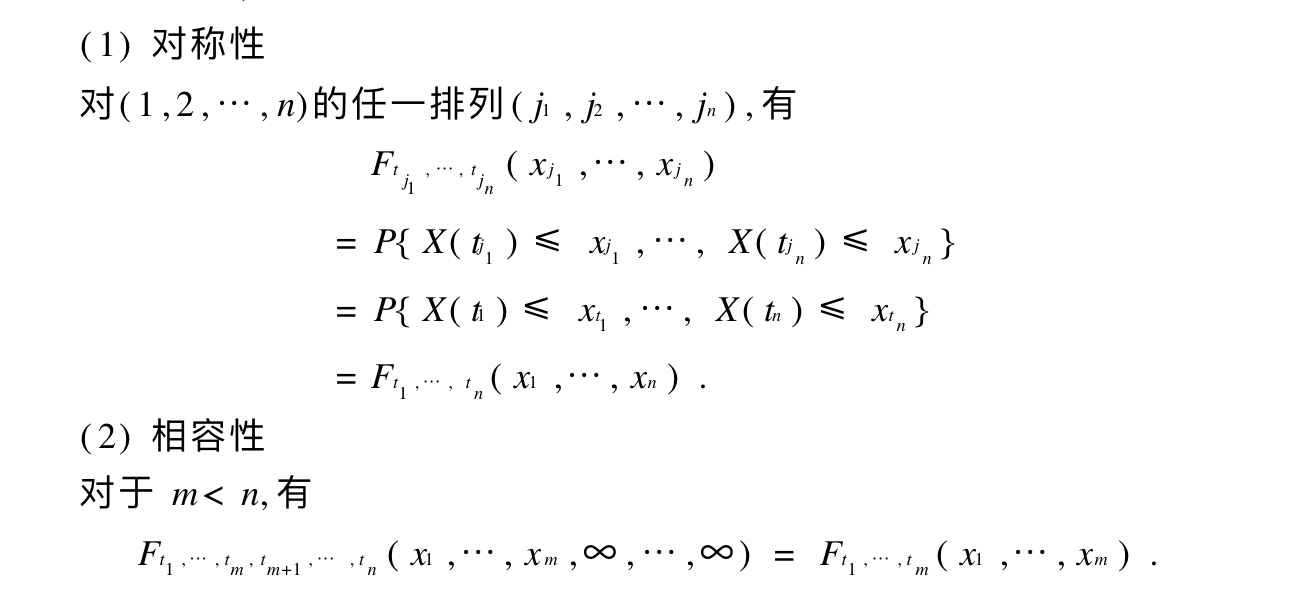

Def: finite joint distribution

Qua: => some qualities

Qua: kolmogov => exist

Note:

1.3. special function

1.3.1. expectation

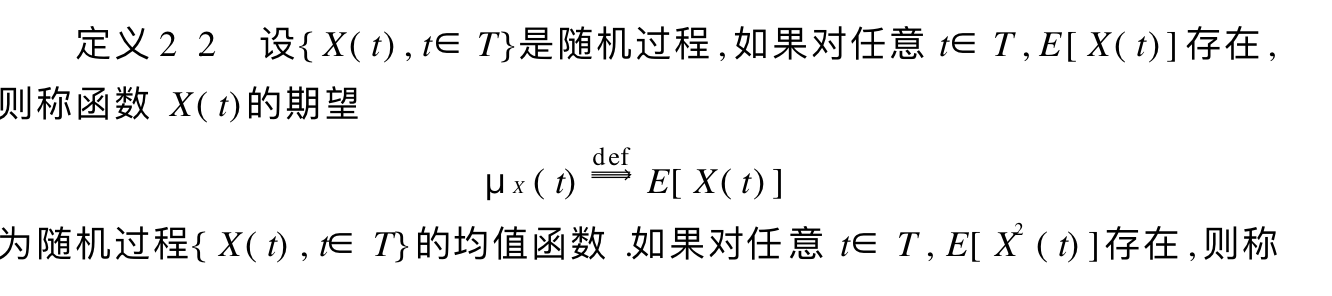

Def: expectation & 2 moment process

Qua: => that co-var & autocorrelation exist

1.3.2. variance

Def: variance

1.3.3. co-variance

Def: co-variance

1.3.4. autocorrelation

Def: autocorrelation

1.4. integration

Def:

Qua: =>

Def:

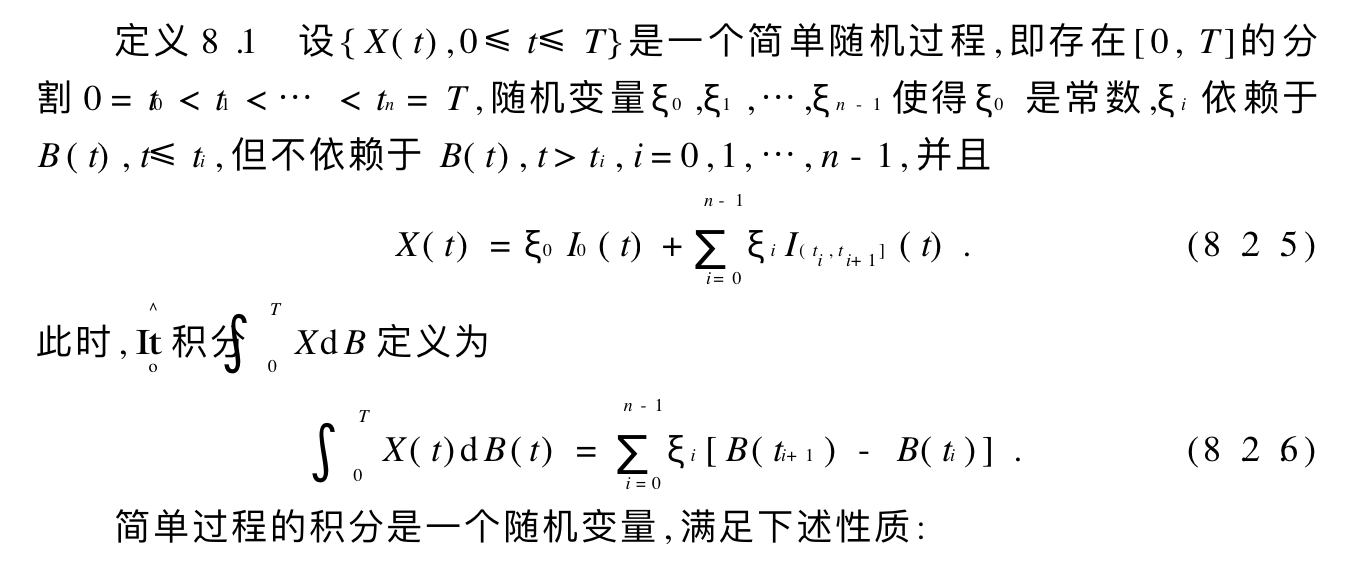

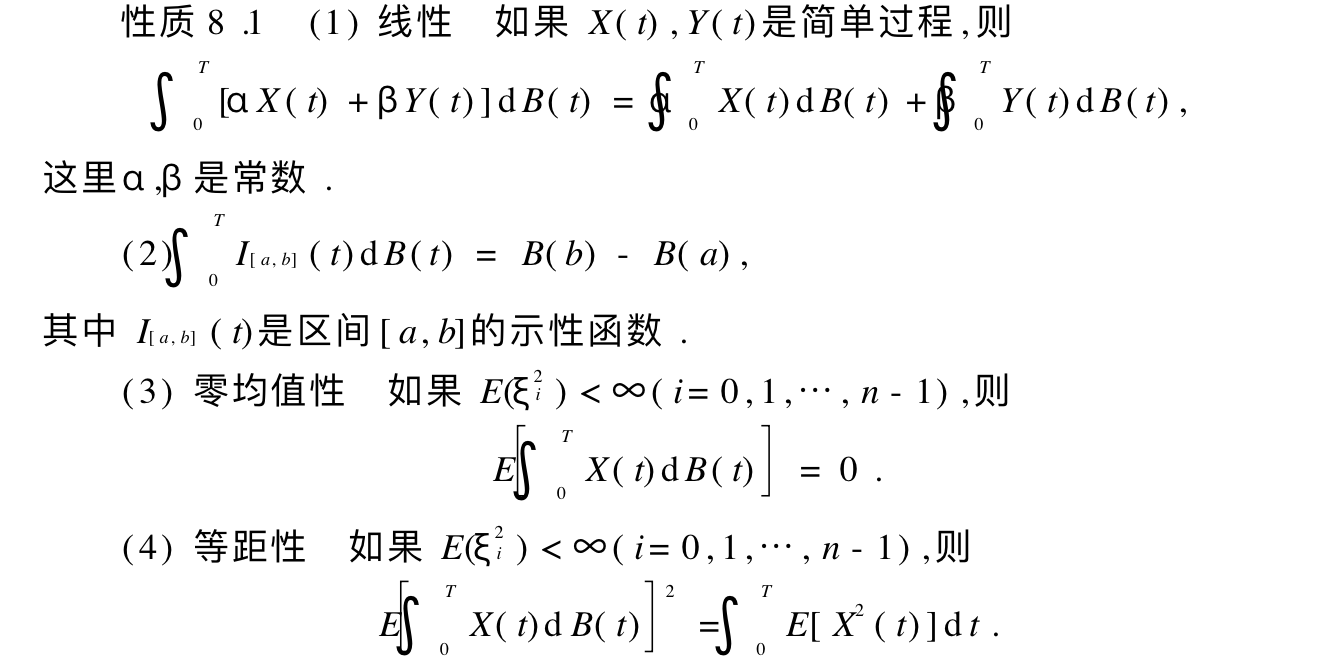

1.4.1. It integral

Def:

Theorem:

Corollary:

Theorem:

Def:

Theorem:

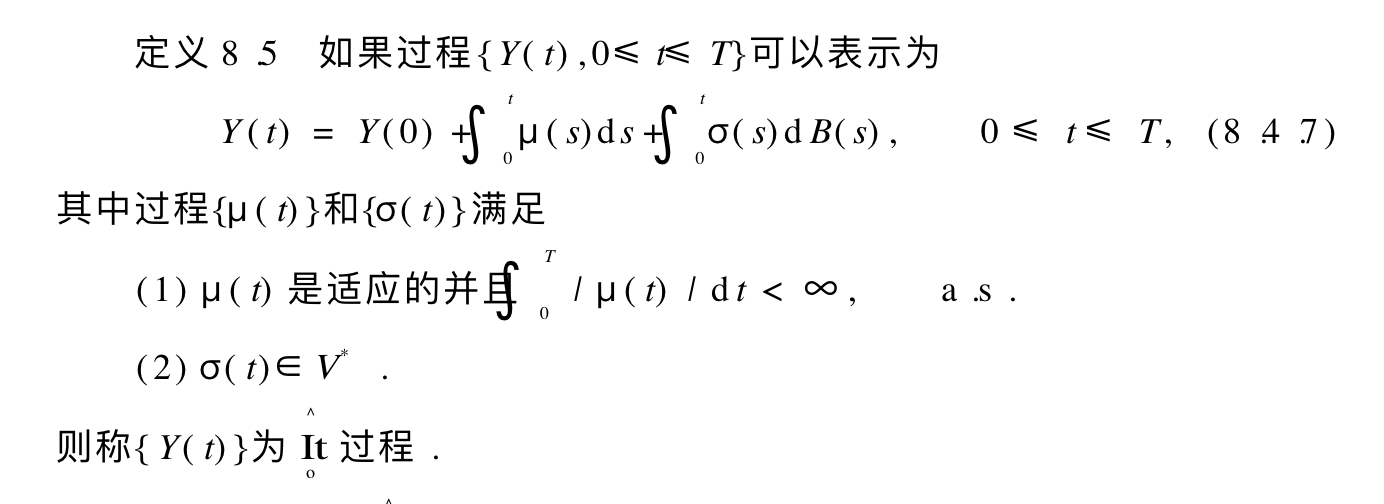

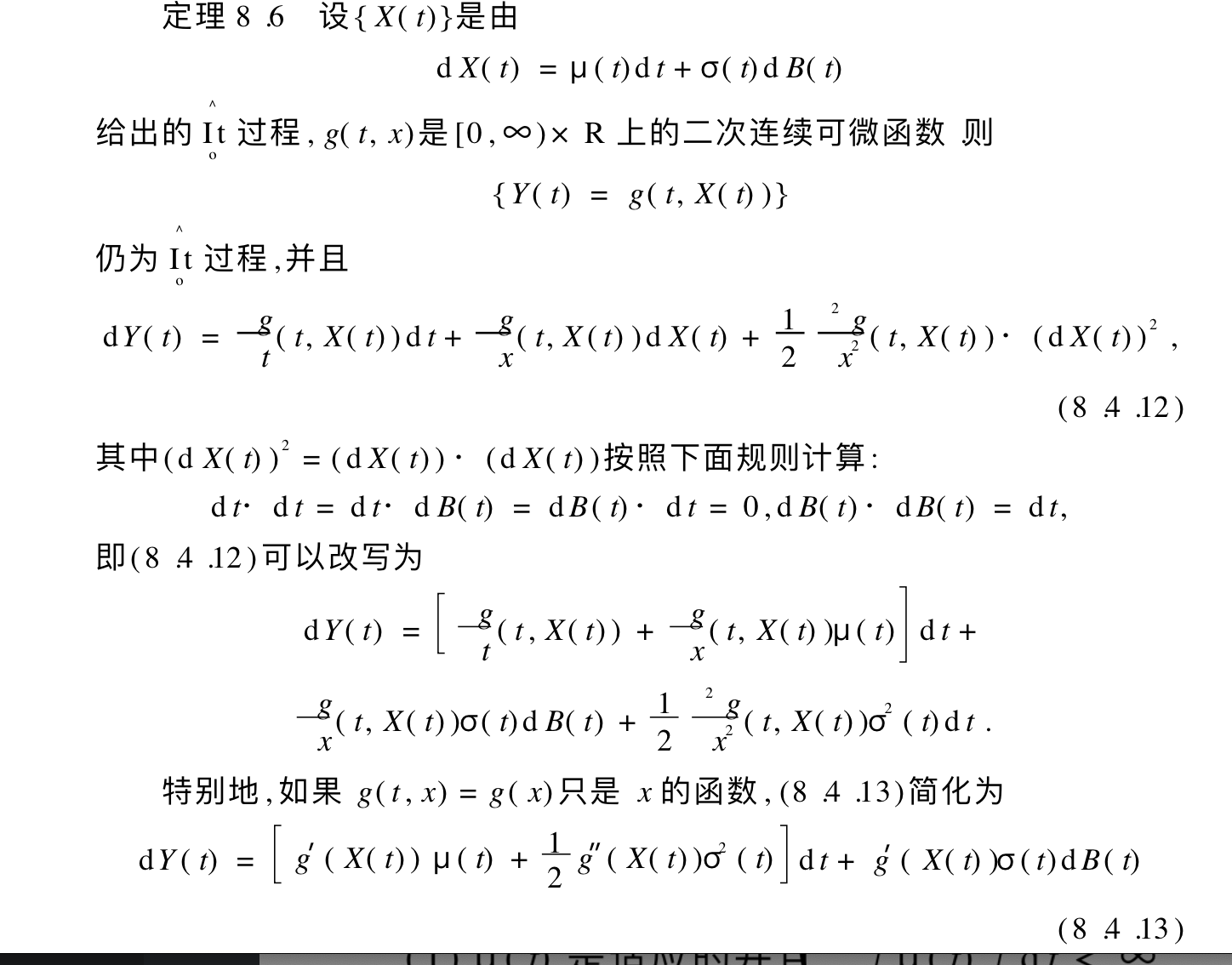

1.4.2. It process

Theorem:

Theorem:

Def:

Theorem:

2. useful processes

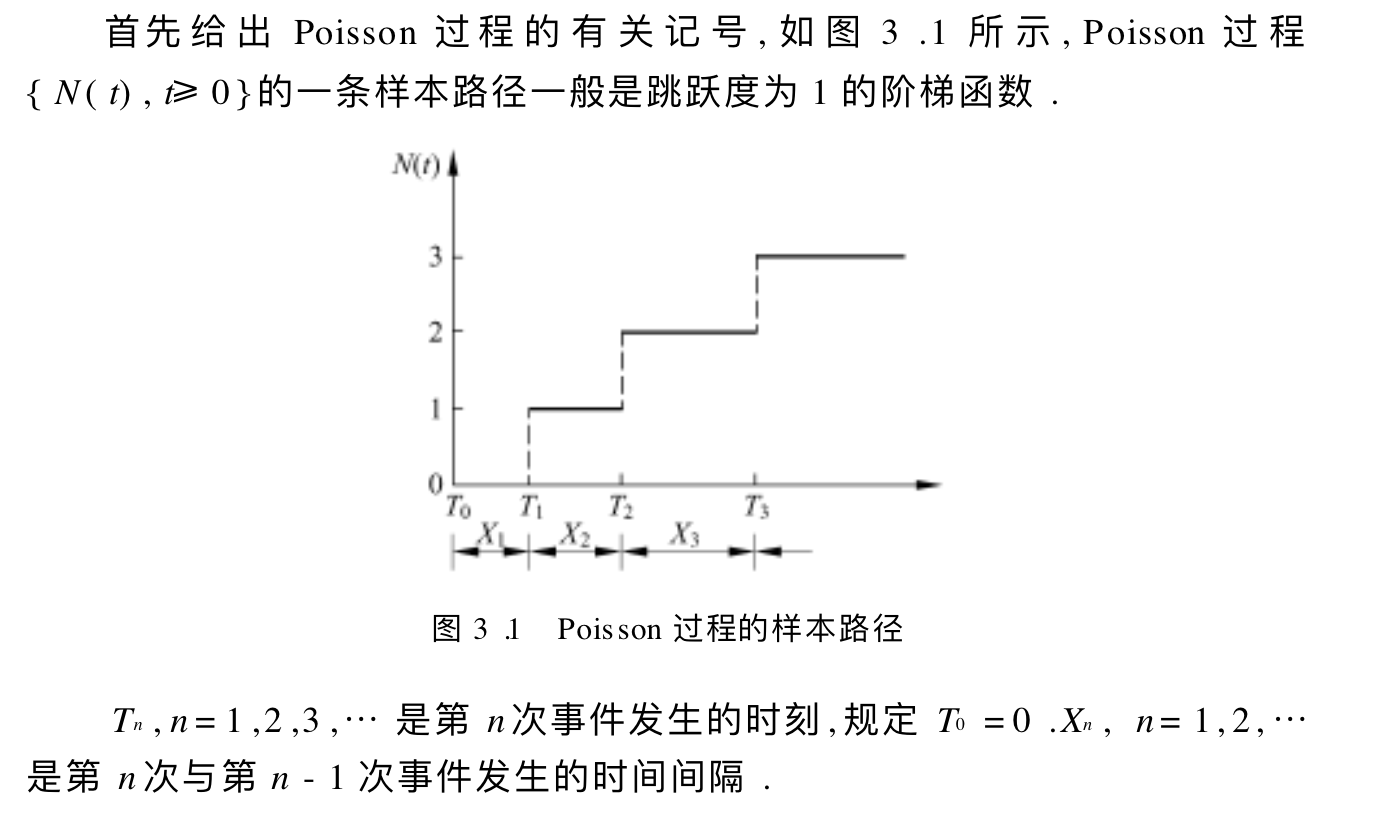

2.1. poisson

Def: counting process

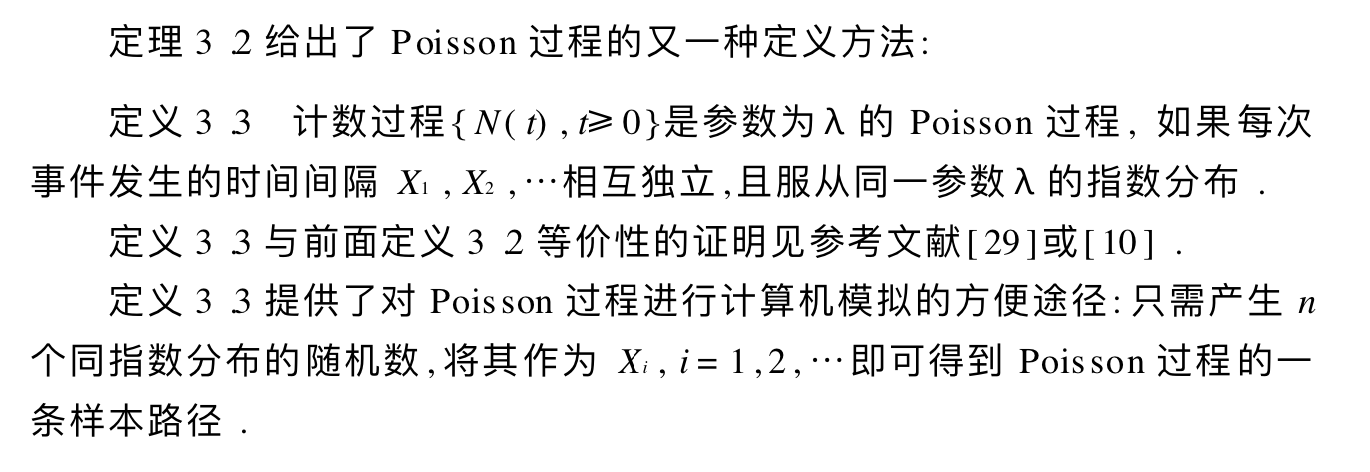

Def: poisson process

Note:

Qua: necc & suff

Qua: necc & suff

Qua: Xn distribution =>

Note:

Qua: tn distribution =>

Qua: tn conditional distribution =>

2.1.1. inhomogeneous poisson

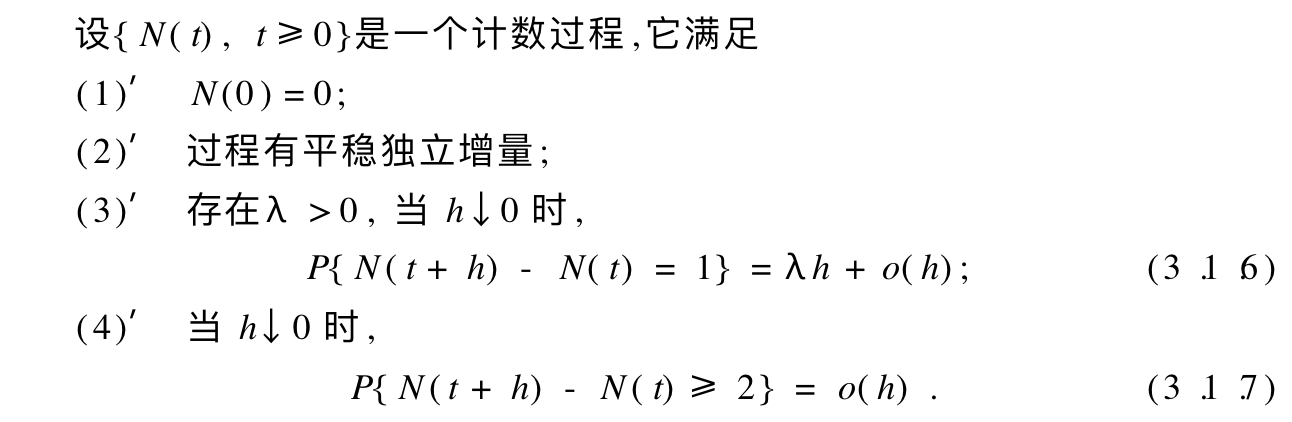

Def; inhomogeneous possion

Qua: necc & suff

Qua: transition with normal =>

Note:

2.1.2. complex poisson

Def: complex poisson

Note:

Qua: => property

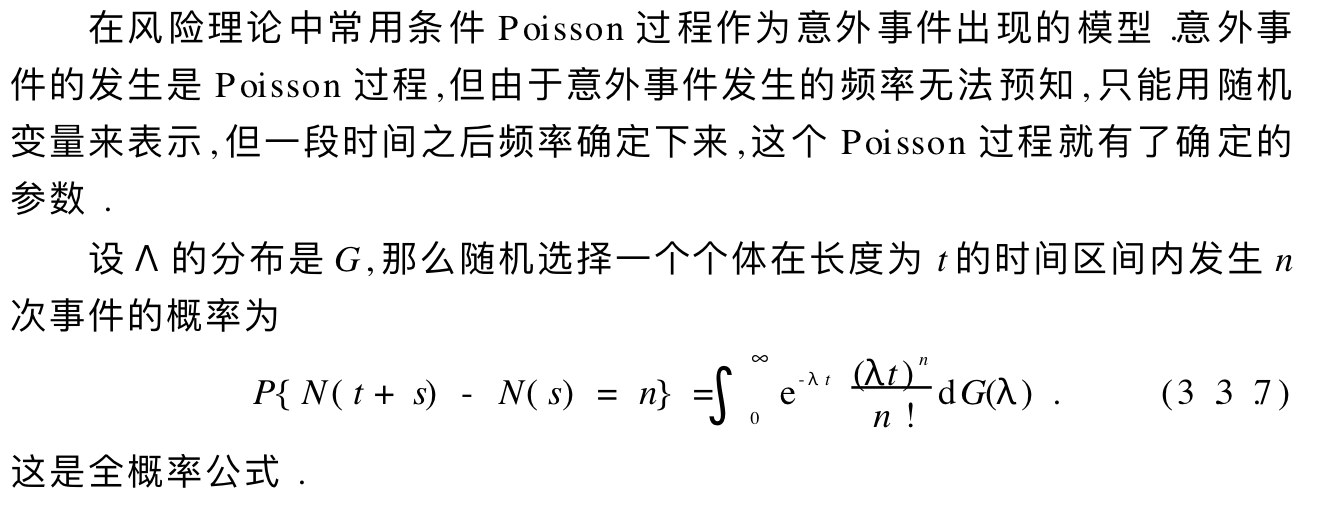

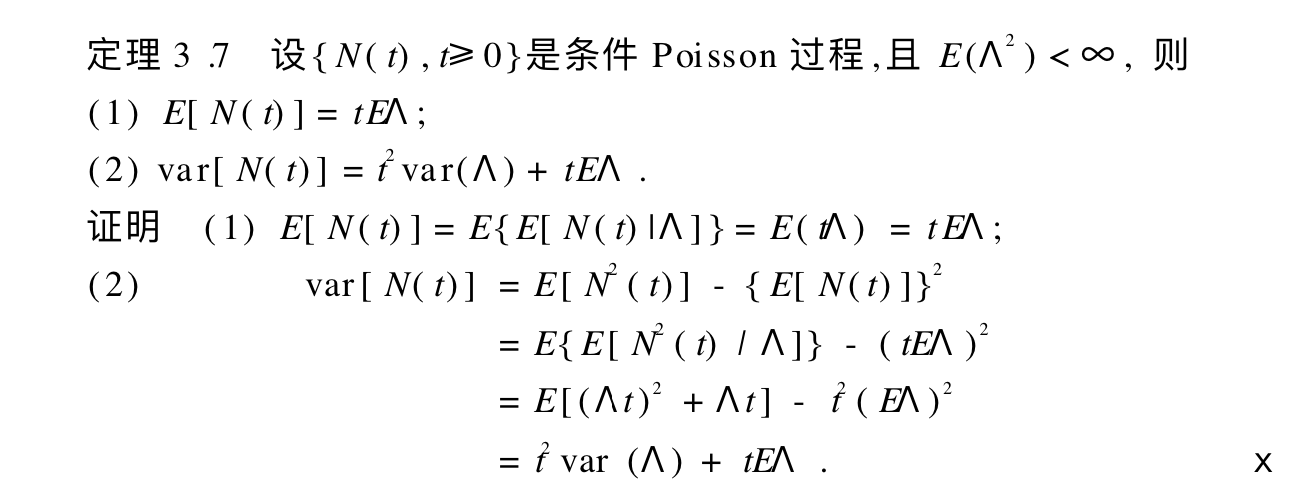

2.1.3. condition poisson

Def; condition poisson

Note:

Qua; => e & var

2.2. brown

Def:

Qua: necc & suff

Note:

Def: inhomo brown

Def:

Qua: =>

Qua: =>

2.2.1. martingale

Theorem:

Note:

2.2.2. markov

Theorem:

Def:

Theorem: strong markov

2.2.3. maximum

Def:

2.2.4. generlization

2.2.4.1. brown bridge

Def:

2.2.4.2. efficient absorb brown

p173

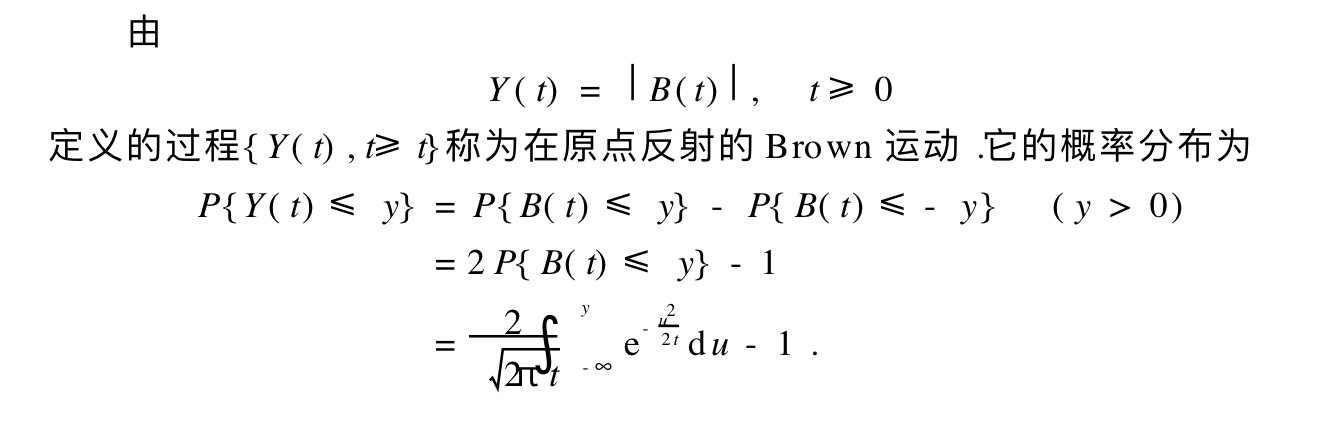

2.2.4.3. reflected brown

Def:

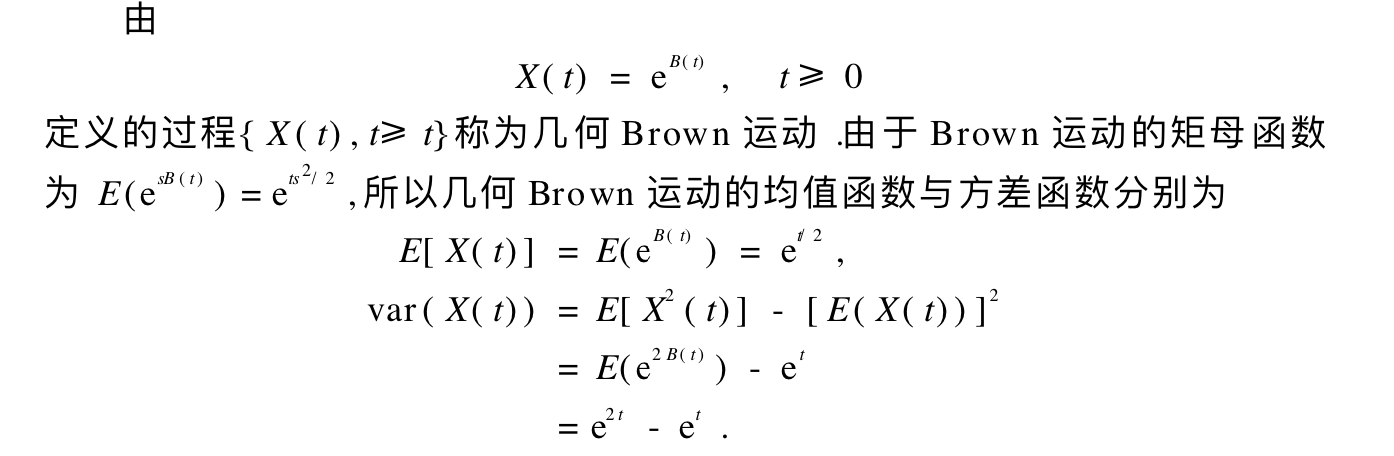

2.2.4.4. geometry brown

Def:

2.2.4.5. shifted brown

p 180

2.3. Gauss

Def: gauss process

3. relationship of stochastic process

## special function

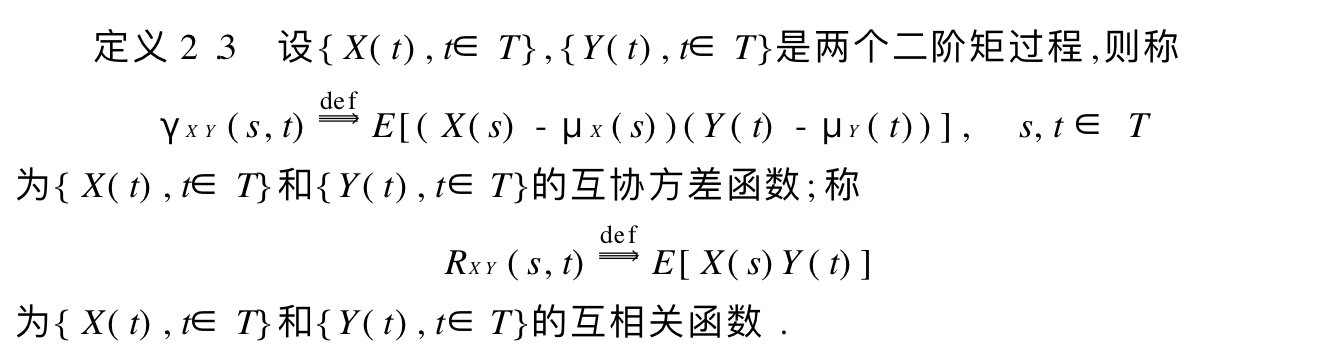

3.0.1. cross-covariance

Def: cross-covariance

3.1. correlation

Def: correlation