Probability Theory Notes

1. frequency & probability

1.1. probability space

1.1.1. Kolmogorov’s probability model

Def1.7: probability space (\(\Omega\), \(\mathscr{F}\), P) ,

Usage: is a special kind of measure space, see for more details. https://blog.csdn.net/tankloverainbow/article/details/102872112

Example: finite sample spaces

Example: infinite sample space

Def1.8: \(P=F ( \mathscr{F} -> R )\), is a finitely additive set function, a measure.

Qua1.9: => Non zero

Qua2.0: => P(must) =1

Qua2.1: => linear

s.t AB does not overlap:

P(A+B) =P(A)+P(B)

1.1.2. special probability spaces

1.1.2.1. frequency norm

Def1.1: frequency of A (A is a 0-1 variable), frequency is a way to depict clasiical probability \[ F _{N}(X) = \frac{n}{N} \]

- Qua1.2: => non-negative:

\[ F _{N}(X) \geq 0 \]

Qua1.3: => regularity:

s.t. X must happen

Qua1.4: => addable:

s.t. A B doesnot happen at once ( A B does not equal 1 at once)

\[ F _{N}(A+B) = F _{N}(A) + F _{N}(B) \]

1.1.2.2. classic norm

Def1.5: classic norm is a special probability space

We set eventspace to be finite, then we define P: where P(event) is \(1/|eventspace|\) regardless of their differences.

1.1.2.3. geometry norm

Def1.6: geometry norm is a special probability space

We set eventspace to be infinite, the rest is same as classic norm.

1.1.2.4. n-Bernoulli norm

Def1.7: is a special probability space

sample = {w1~n} (n bernoulli 0/1)

samplespace = {\(2 ^{n}个sample\)}

P({X=k}) = \(C(n,k)p^k(1-p)^{n-k}\)

1.2. conditional probability

1.2.1. conditional prob

Def1.7: conditional prob

s.t $P(B) 0 $ \[ P(A|B) = \frac{P(AB)}{P(B)} \]

1.2.2. all prob equation & bayes equation

Def1.8: complete event group \(\left\{ A1, A2,...An \right\}\) \[ (1) Ai \; not \; overlap \\ (2) P(Ai) >0 \\ (3) \sum_{n = 1}^{\infty}Ai = ALL \]

Theorm1.8: all prob equation

s.t. \(\left\{ A1, A2,...An \right\}\) is complete event group \[ P(B) = \sum_{n = 1}^{\infty}P(A_i)P(B|A_i) \]

Theorm1.9: bayes equation

s.t. \(\left\{ A1, A2,...An \right\}\) is complete event group \[ P(A_i|B) = \frac{P(A_i).P(B|A_i)}{\sum_{k = 1}^{\infty}P(A_k).P(B|A_k)} \]

Def1.10: priori prob \[ P(A_i) \]

Def1.11: posteriori prob \[ P(A_i|B) \]

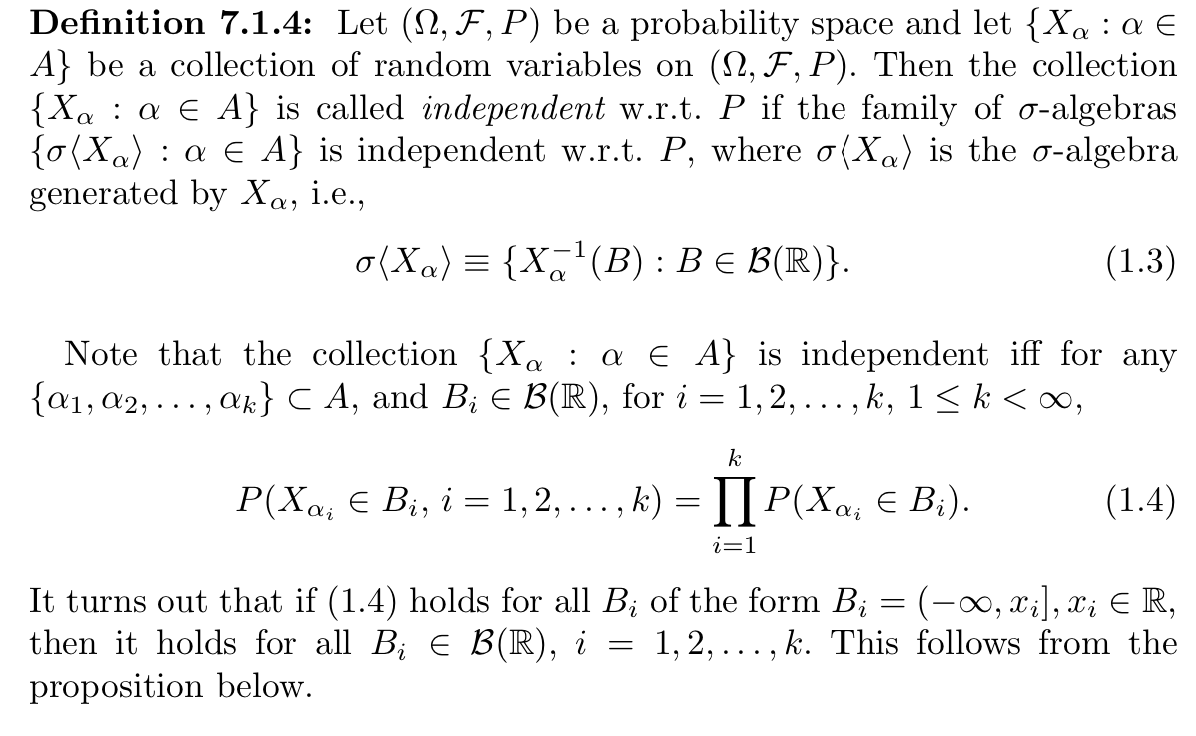

1.2.3. independence (of event)

Def1.12: dependence of collection of event

Def: dependence of collection of event

Def: dependence of collection of event

1.3. L2 space

Def:l2 space

Qua: => hilbert

Proof:

2. random variables

2.1. distributions

Def: random variable X is a measurable function, F(samplespace to R)

Usage: distributions are determined by 2 factors: X and P, since we do not know P, so we do not accutually care if random variable is defined on the same Probabilty space or not, they can be or they can not.

Def: discrete / continuous random variables

Note: other definitions

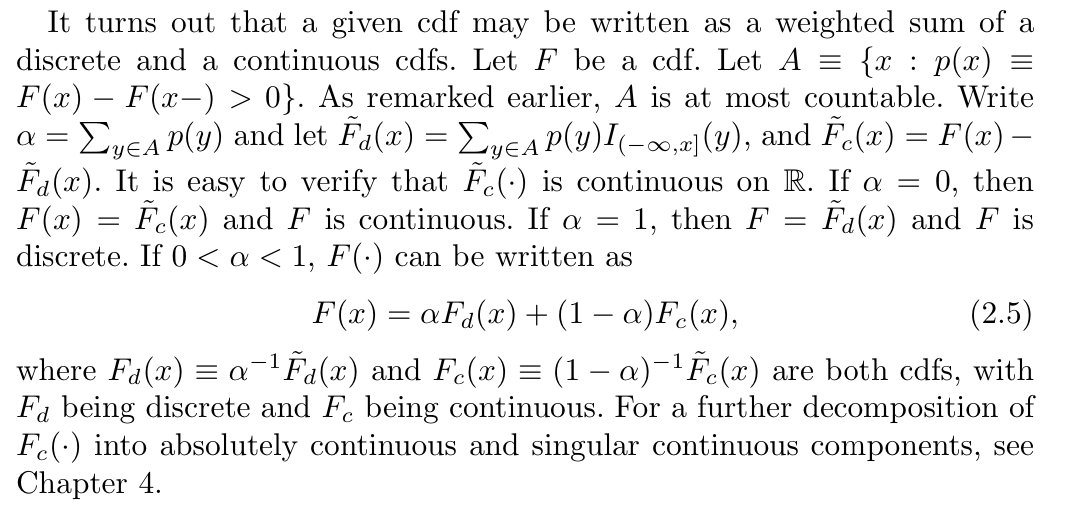

Note: decomposition of F(x) if X is neither continuous nor discrete

2.1.1. pdf

Def: Probability Distribution of X(w)

Usage: a induced measure from R to $ $

Def2.6: Probability Density Function of X(w) \[ p _{X}(k) = F _{X}'(k) \]

Qua2.7: => single point $$ \[\begin{align} P(X=k) &= F(k)-F(k-0) \\ &= \lim_{h \to 0+} \int_{k-h}^{k}p(y)dy \\ \end{align}\] $$

Qua2.8: => non-negative \[ p _{X}(k) \geq 0 \]

Qua2.9: => regularity \[ \int_{n = - \infty}^{\infty}p_{X}(y)dy =1 \]

2.1.2. cdf

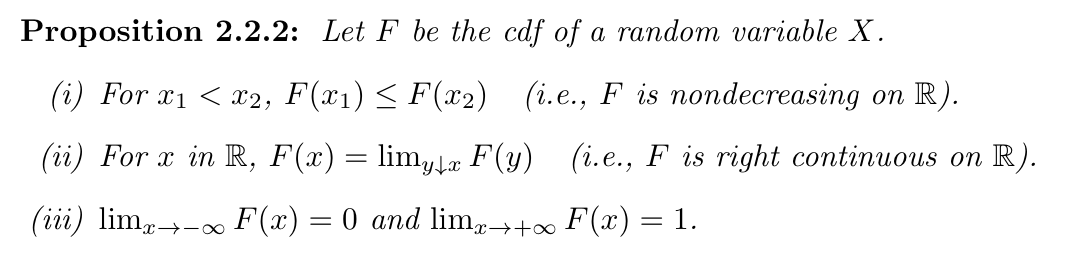

Def2.2: Cumulative Distribution Function of X(w) (cdf)

\[

F _{X} (k) = P(X \leq k) = \int_{- \infty}^{k}p_{X} (y)dy

\]

\[

F _{X} (k) = P(X \leq k) = \int_{- \infty}^{k}p_{X} (y)dy

\]Qua: necc & suff

2.2. special functions

2.2.1. expectation

Def1.1: expectation of random variable

s.t. (1) \[\sum_{k}^{} |k|*P_(X=k) < \infty\] \[ Func(X)=E(X)=\sum_{k}^{} k*P_(X=k) \\ Func(X)=E(X)=\int_{k} k*p_X(k) dk \\ Func(X)=E(X) =\int_{\Omega}X(w)dP(w) \]

Qua1.2: some useful expectations

Qua1.3: => monotonicity

s.t. $ a X b $ \[ (1) E(X) \exists \\ (2) a \leq E(X) \leq b \]

Qua: => monotonicity

s.t. (1) \(|X| \leq Y\)

(2) $E(Y) $

\[ E(|X|) \exists \]

Qua1.4: => linearity (E into sumation)

s.t.$Ex1, Ex2...Exn $ \[ E( \sum_{n = 1}^{\infty}ciXi+b) =ci \sum_{n = 1}^{\infty}E(Xi)+b \]

Qua1.6: => limitation (bound and convergence)

s.t. (1) \(\lim_{n \to \infty}X _{n}(w)=X(w)\)

(2) for all \(n \geq 1\), \(|X _{ n}| \leq M\) \[ \lim_{n \to \infty}E(X _{n}) = E(X) \]

Qua1.11: operation

s.t. (1) g(x) is borel function

\[ Eg(X) = \int_{- \infty}^{\infty} g(k)p_X(k)dk \]

Qua1.12: => steins theroy

s.t. (1) X~N(0,1)

(2) g is continuous & derivable

(3) \(E|g(X)X|< \infty\)

(4)\(E|g'(X)|< \infty\) \[ E|g(X)X|=Eg'(X) \]

2.2.2. variance

Def: Bias ( is a metric of approximation X to a ) \[ Bias( \hat{X},a )= E( \hat{X})- a=number(\hat{X}) \]

Def: MSE ( is a metrics of approximation) \[ MSE(\hat{X} ) =E(\hat{ X} - a) ^{2} = V(\hat{X})+Bias^{2}(\hat{X},X ) =number(\hat{X}) \]

Def: length \[ Length(\hat{X}) = E||\hat{X}||^2 \overset{when E(\hat{X})=a}{=} MSE(\hat{X})+||a||^2=number(\hat{X}) \]

Def1.13: deviation \[ D(X) = X-E(X)=randonvariable(X) \]

Def1.14: variance

s.t. abs < inf

\[ V(X) = E(D(X)^{2})=E(X-E(X)) ^{2}= E||X||^2-E(X)^TE(X)=number(X) \]

- Qua1.16: => var = 0 means degenerate

- Qua1.17: => quadratic

\[ V(cX+b) = c ^{2}V(X) \]

Qua1.18: => sup

s.t. \(c \ne E(X)\) \[ V(X) < E(X-c)^{2} \]

Qua1.19: => double linearity

\[ V( \sum_{n = 1}^{\infty}Xi)= \sum_{n = 1}^{\infty}V(Xi)+2\sum_{1 \leq i<j \leq n}^{}E(Xi-EXi)E(Xj-E(Xj)) \]

2.2.3. moment

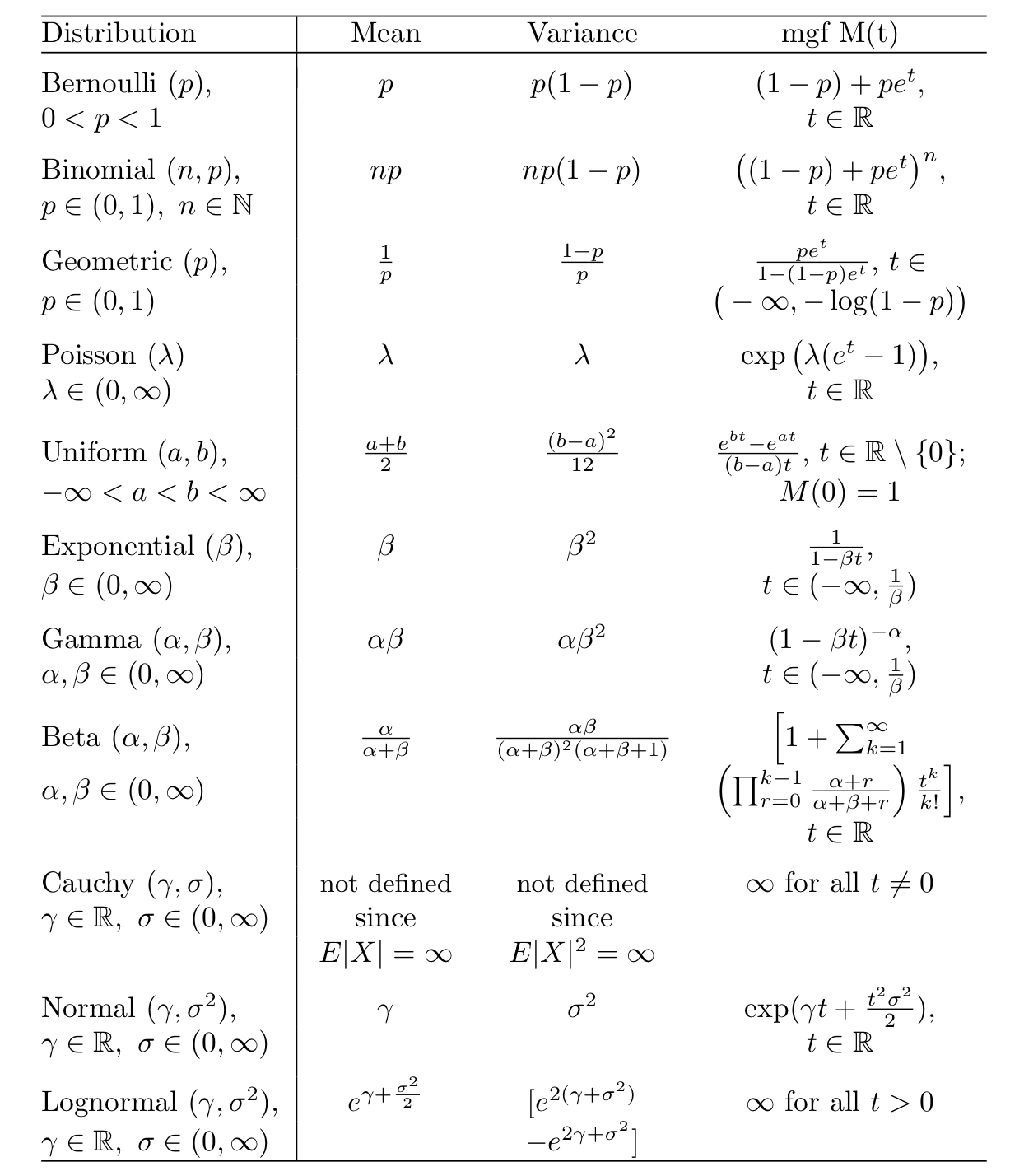

Def2.27: moment, 原点/中心 \[ m_k = EX ^{k}\\ c_k = E(X-EX) ^{k} \]

Qua2.27: => relationship between different moments

Qua2.27: => equatiom

Qua2.27: => moment & cmf

2.2.4. characteristic function

Def2.28: cf

Qua2.29: => 1 on 1

Proof

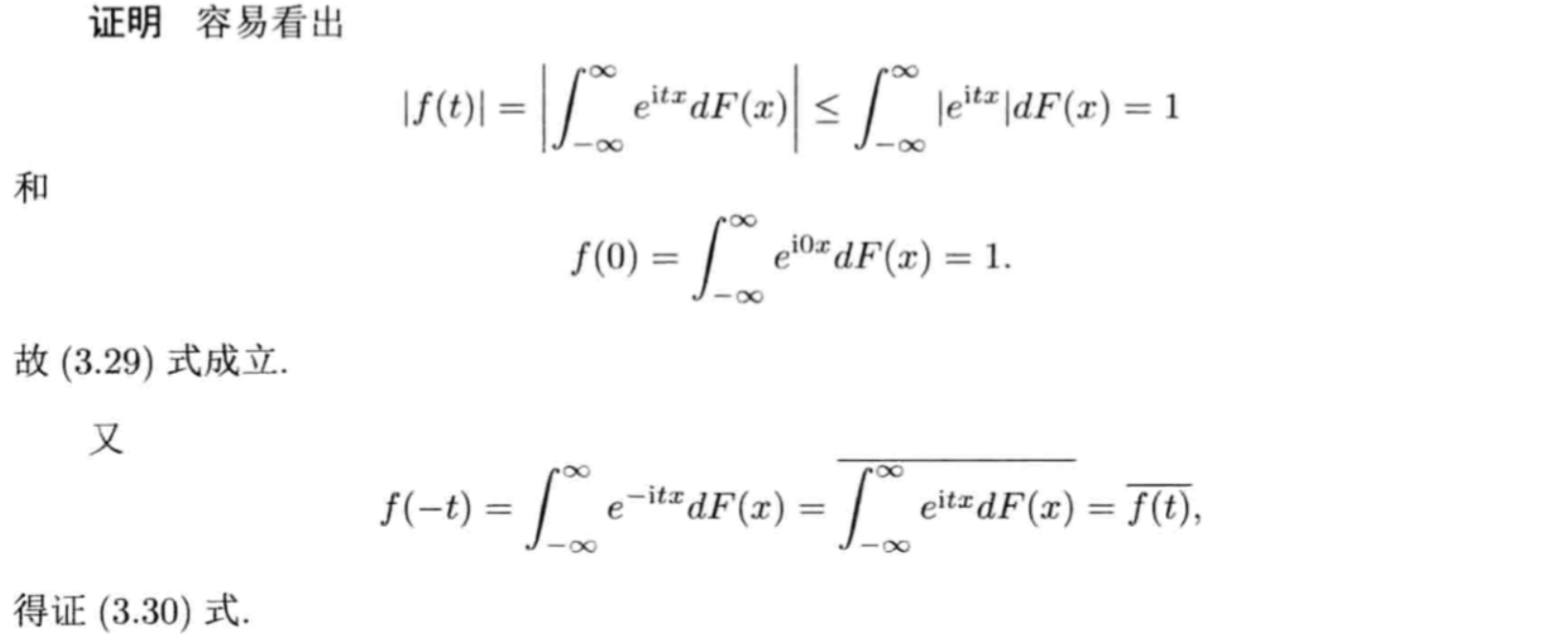

Qua2.30: => 0 is the largest

Proof:

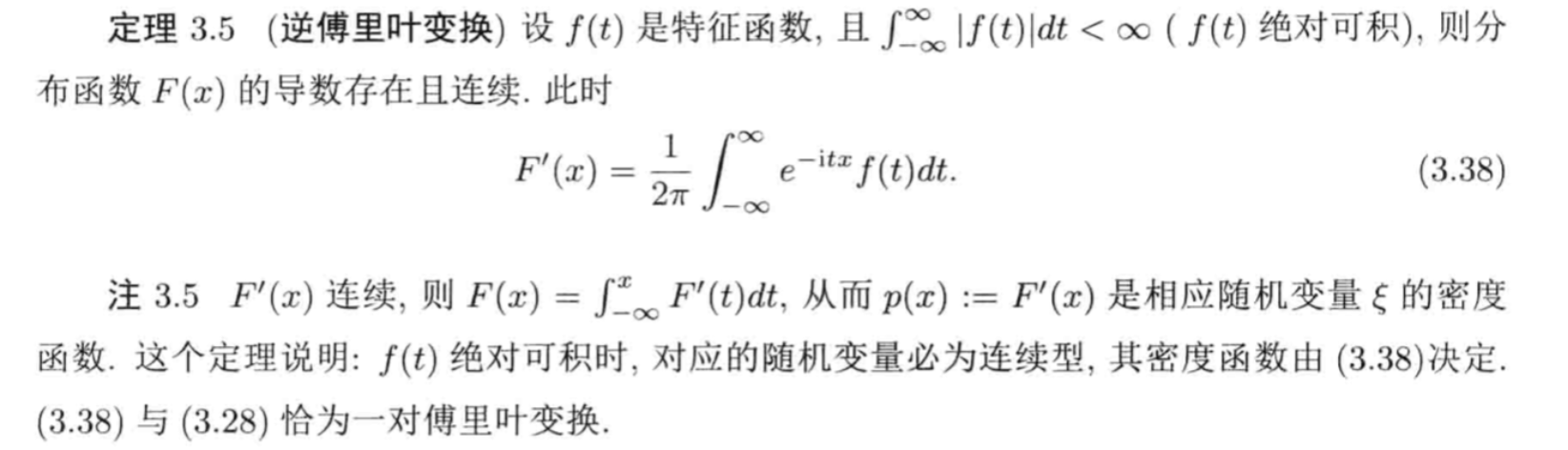

Qua2.31: => 一致continuous \[ f(t) \to -\infty\ , \infty)一致 continuous \] Proof: too long

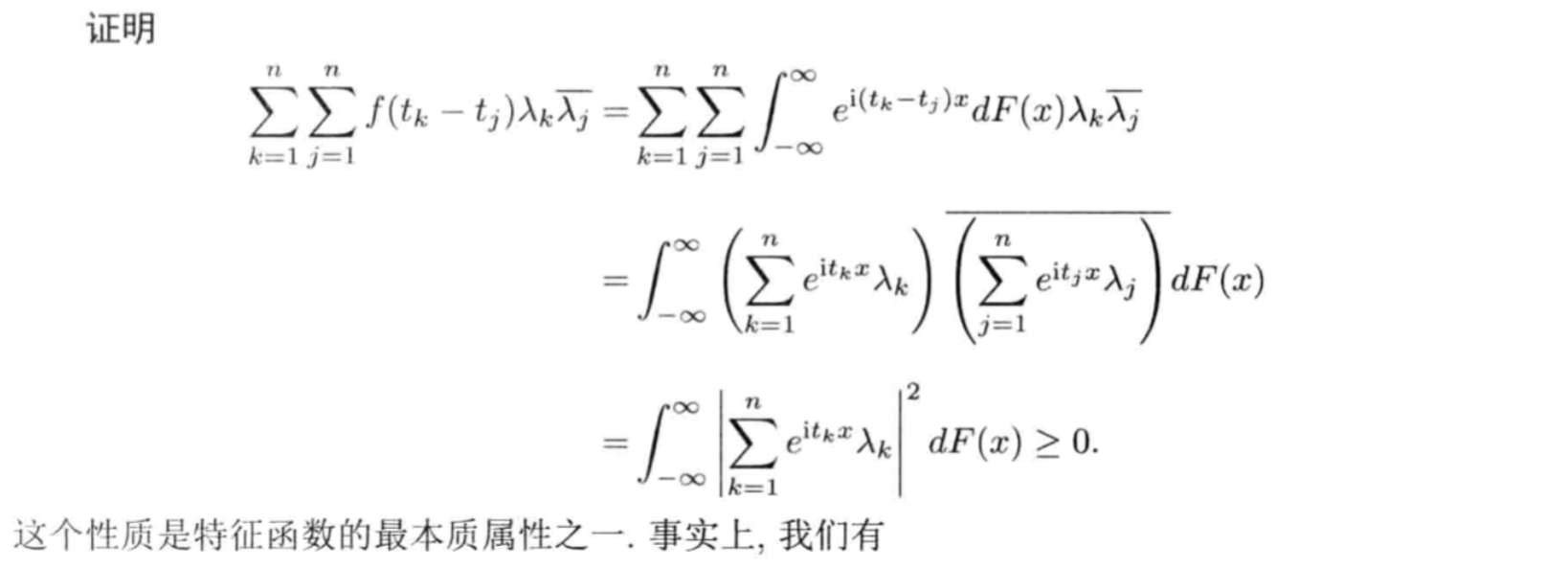

Qua2.32: => 非负定

Proof:

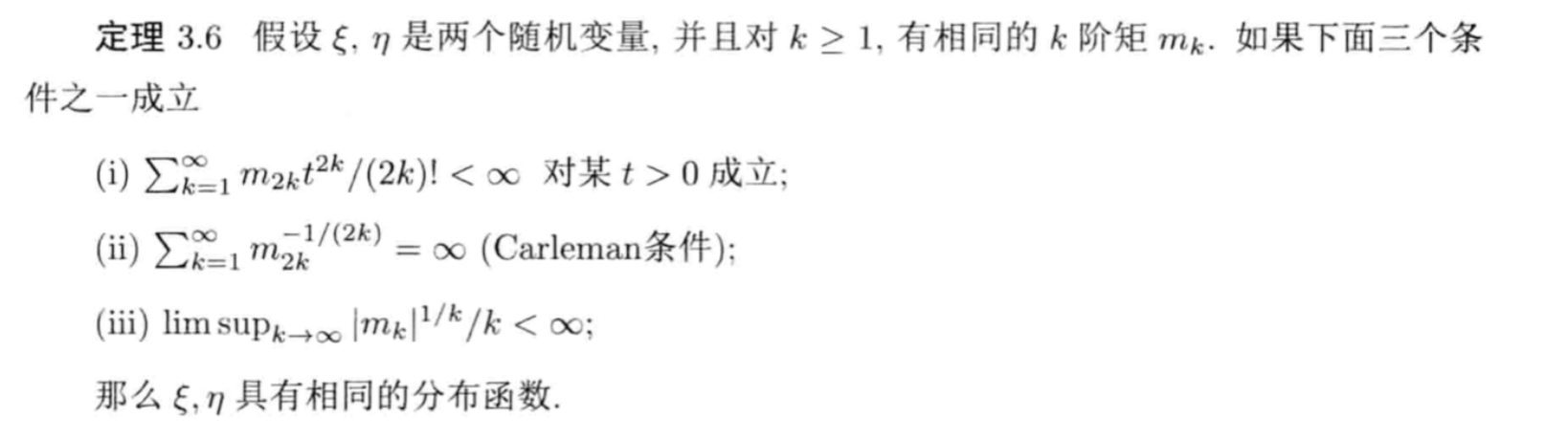

Theorm2.33: Bochner-K, necessary and sufficient condition;

Qua2.34: => Cf & moment

Proof: too long

Qua2.35: => linearity

Qua2.36: => cf & cmf

Proof:

Qua2.37: => cf & cmf

2.2.5. generating function

Def2.38: generating function

Qua2.39~2.42: =>

Qua2.43: => gf & cf

2.2.6. martingale

Def:

Qua: =>

3. relationships of random variables

3.1. conditional & joint

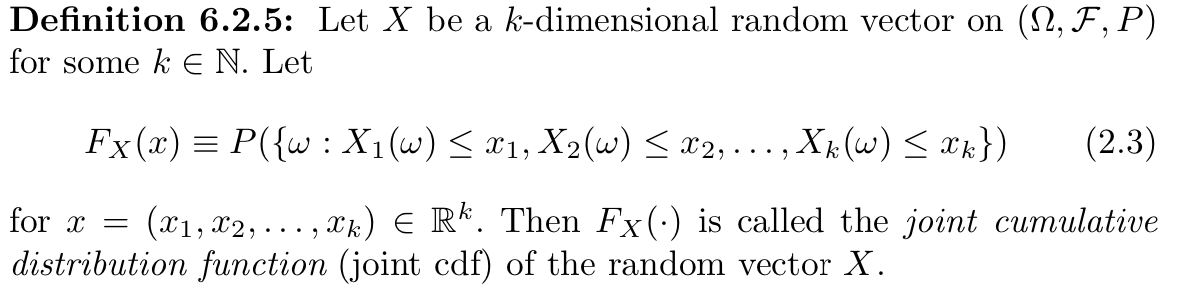

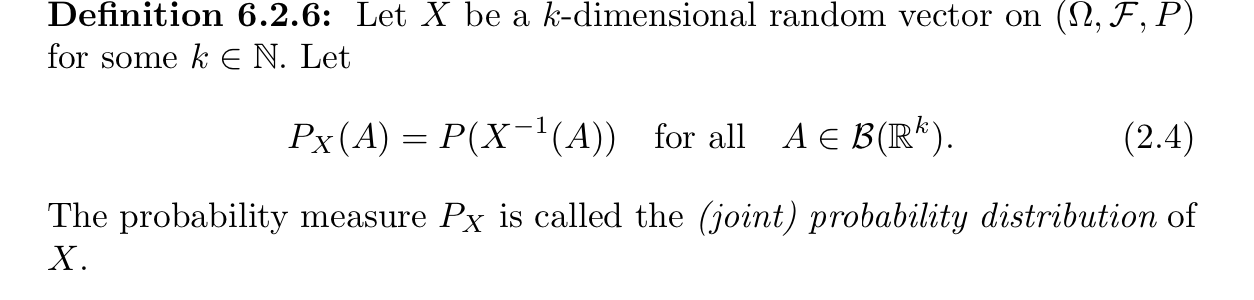

3.1.1. joint distribution

Def: joint cdf

Def: joint pdf

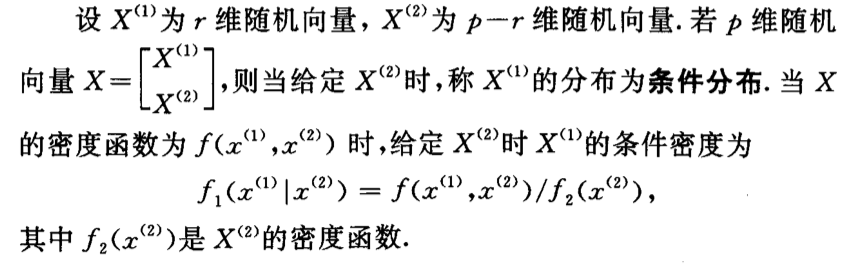

3.1.2. conditional distribution

Def: conditional cumulative function \[ F _{X|Y}(c|b)=P(X \leq c|Y=b) = \sum_{x_i \leq c}^{}p _{X|Y}(x_i|b)=number(c,b,X,Y) \\ F _{X|Y}(c|b)==P(X \leq c|Y=b) = \int_{- \infty}^{c} \frac{p_{X,Y}(v,b)}{p _{Y}(b)}dv=number(c,b,X,Y) \]

Def: conditional density function \[ P _{X|Y}(c|b) = \frac{P(X=c, Y=b)}{P(Y=b)}=number(c,b,X,Y) \\ P _{X|Y}(c|b) = \frac{p_{X,Y}(c,b)}{p _{Y}(b)} =number(c,b,X,Y) \]

Def conditional probability of a event A given random variable X \[ not important \]

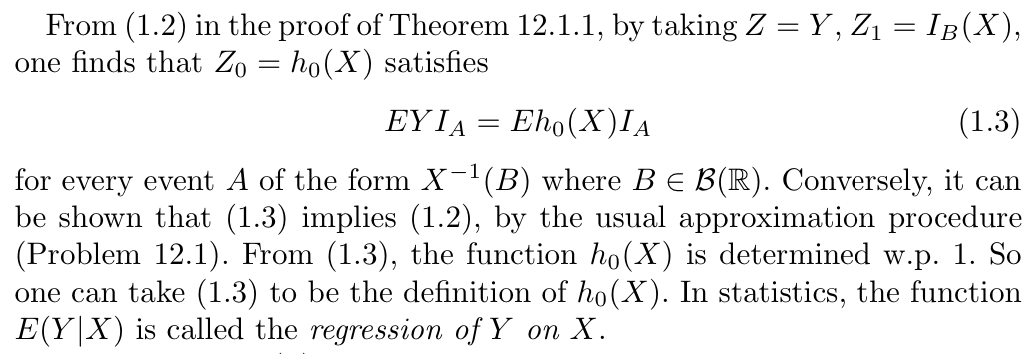

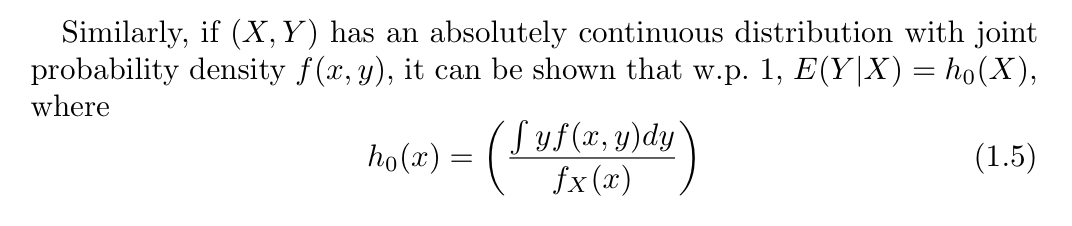

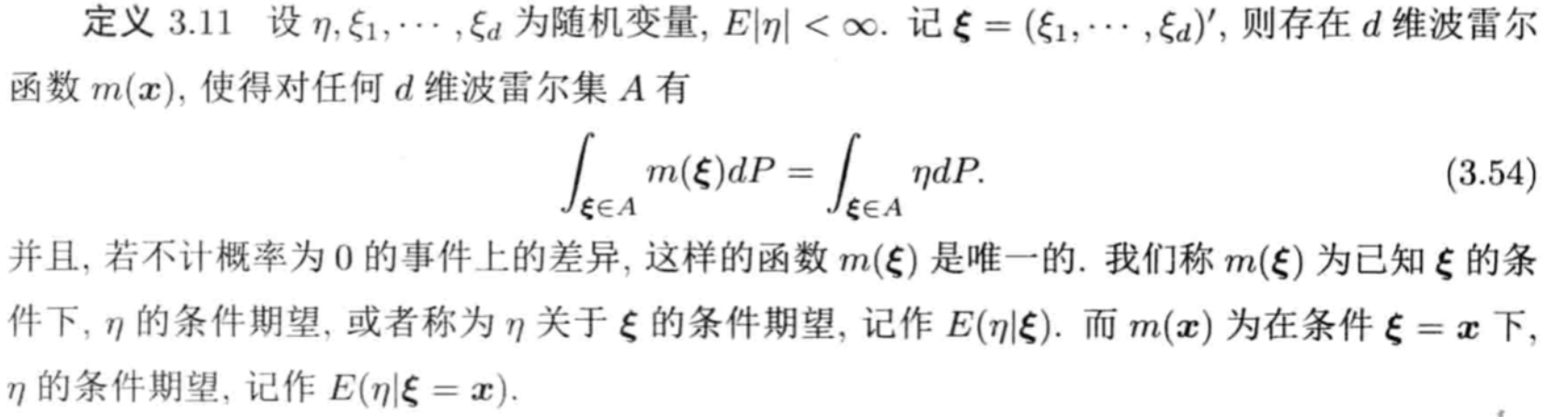

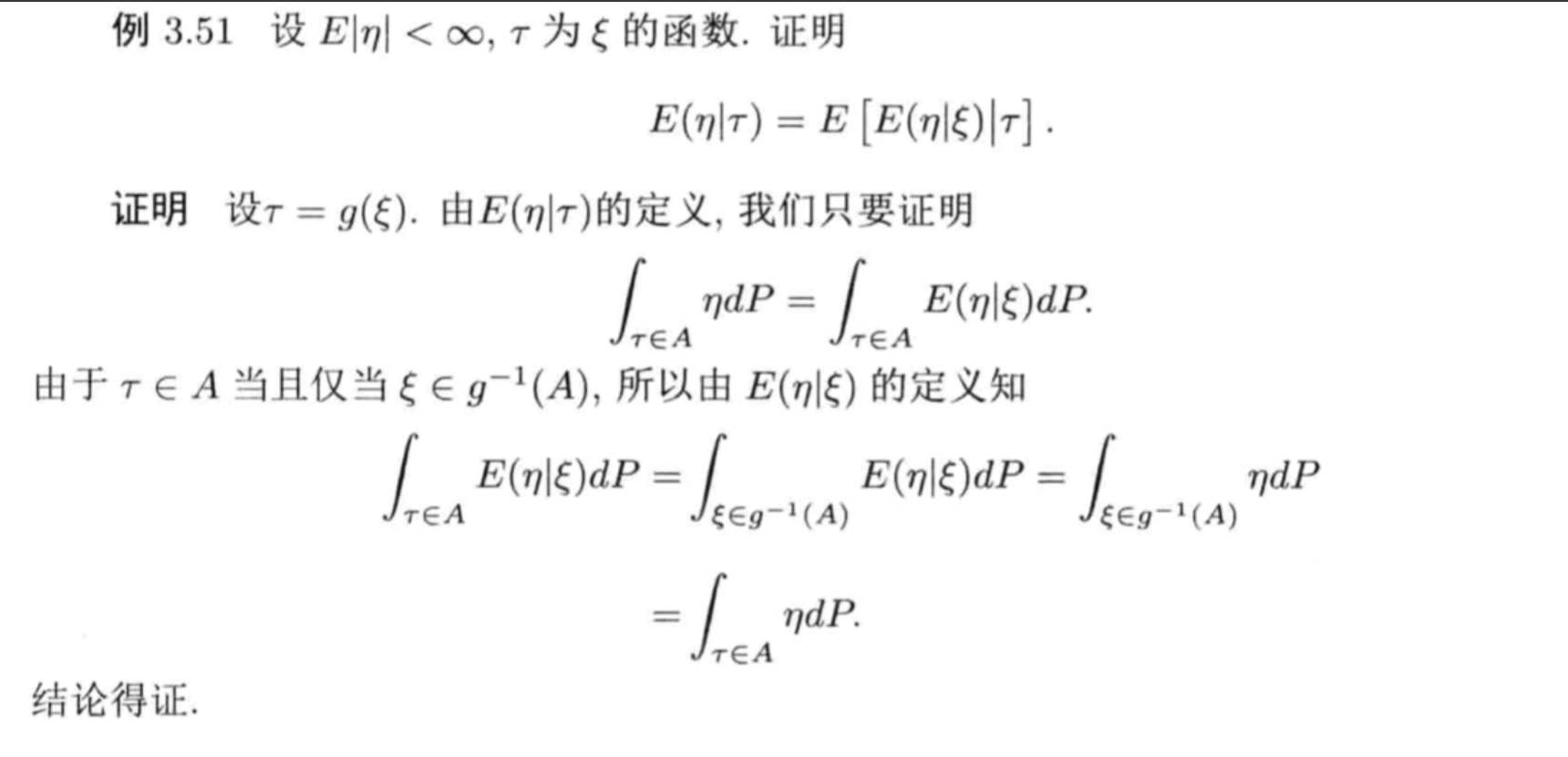

3.1.3. conditional expectation (projection)

3.1.3.1. conditional expectation

Def: conditional expectation of Y given X

Note: other definition

Note: other definition

Note: other definition: also called projection

Example:

case of discrete random variable

case of continuous random variable

Qua: => basic quality

Qua: => some equality (2-4)

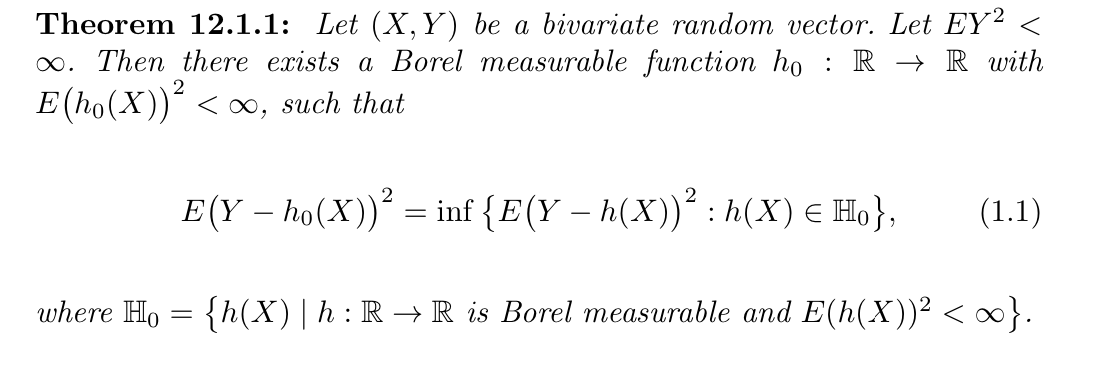

Theorem: => existence

Theorem: (2-4) => equation

Theorem: (2-4) => equation

Lemma: ? (2-4) => equation

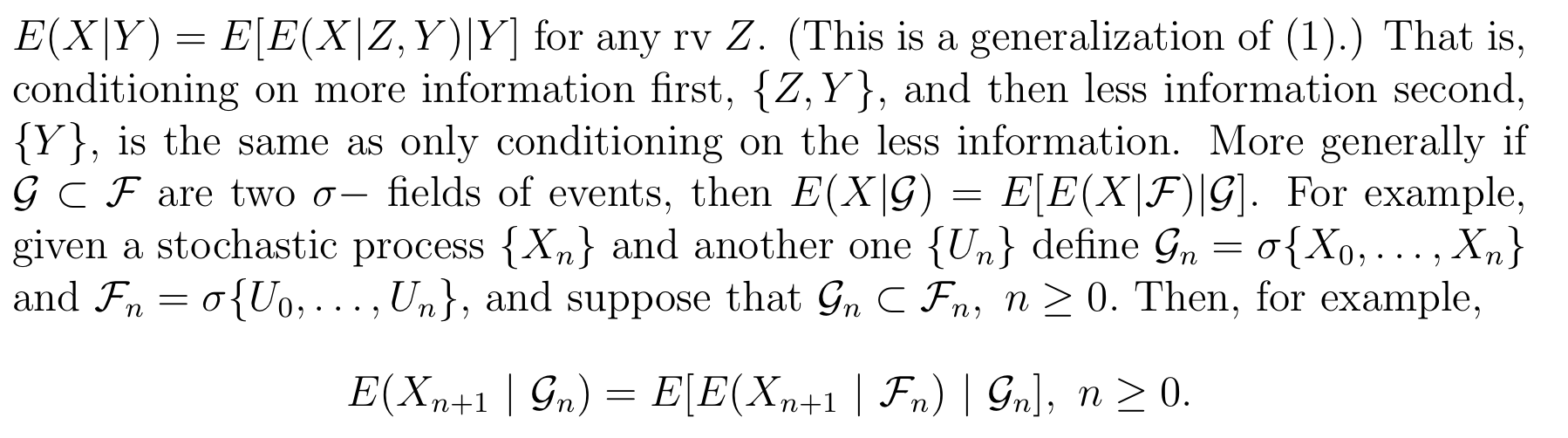

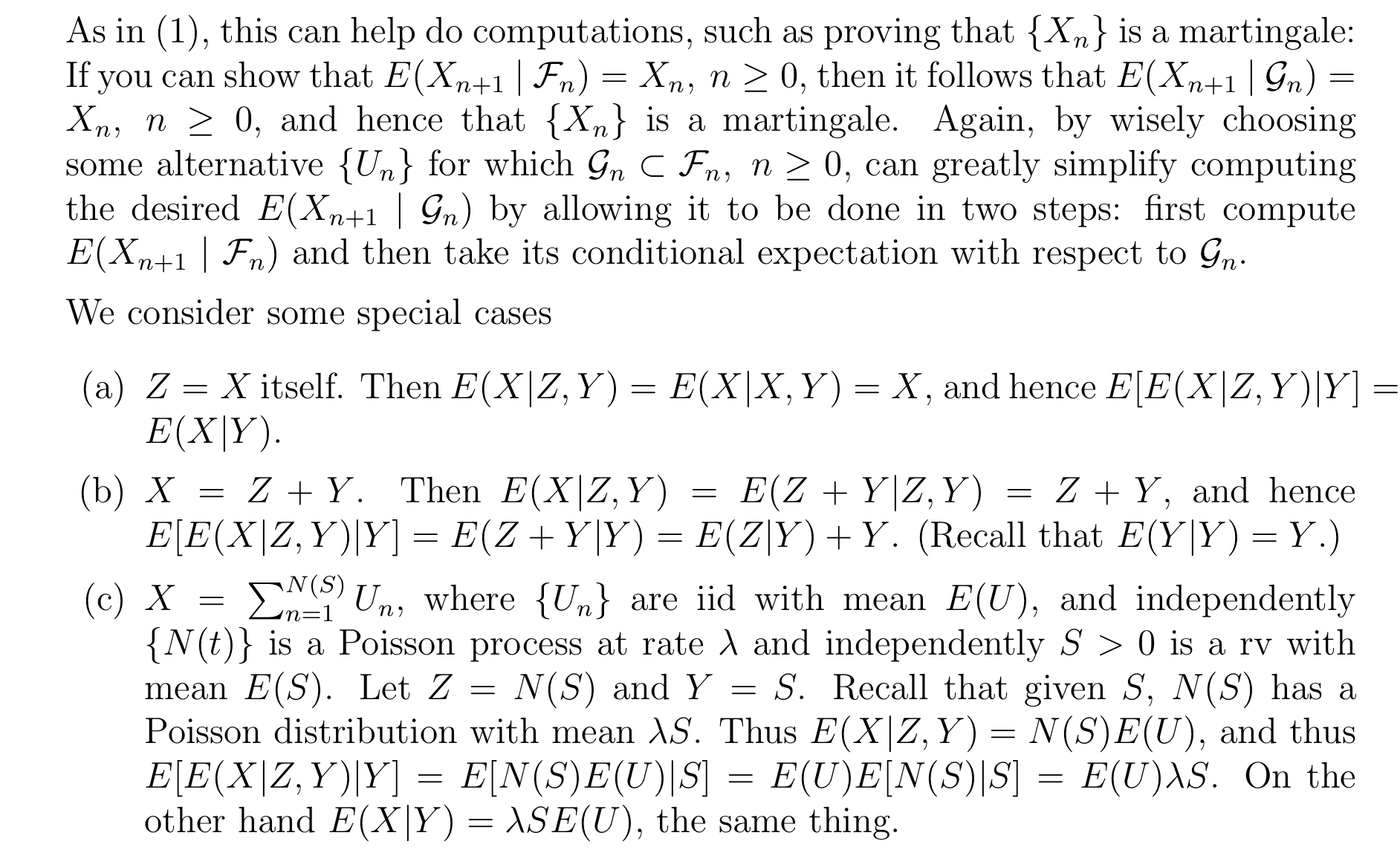

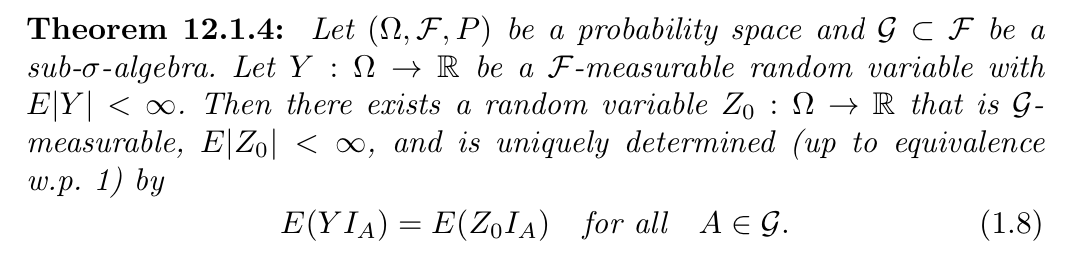

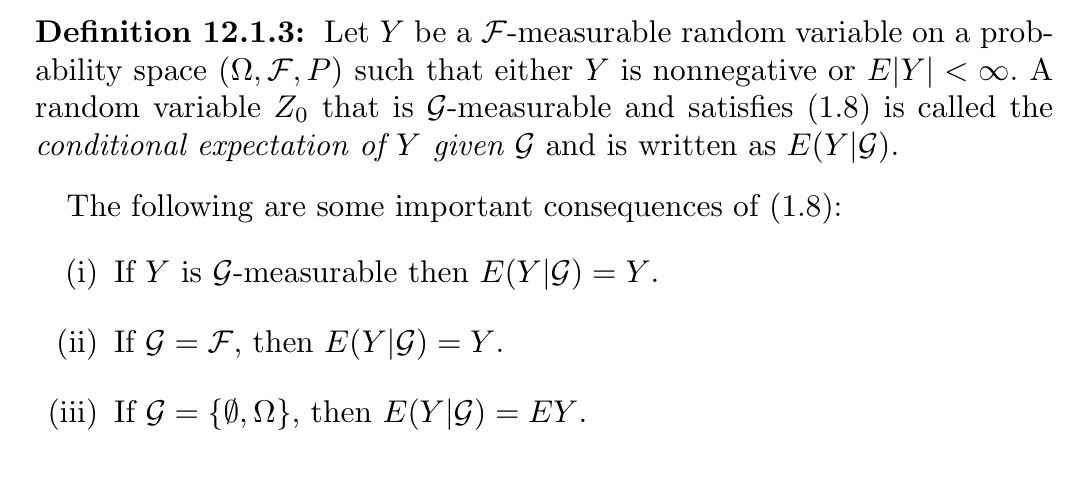

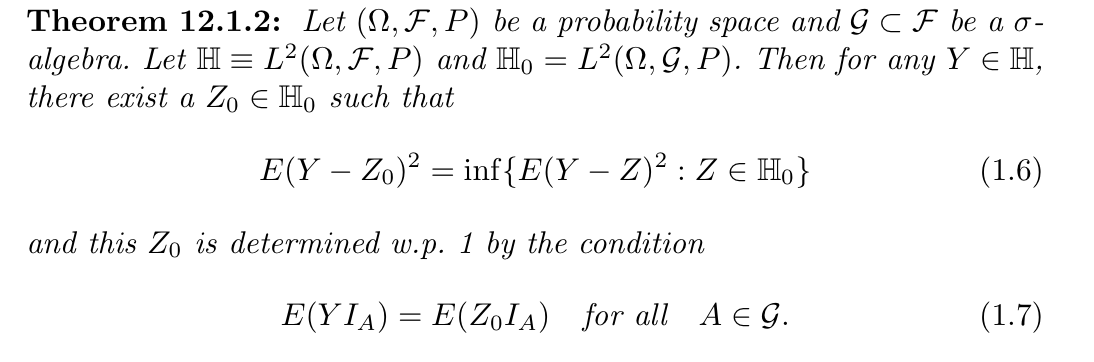

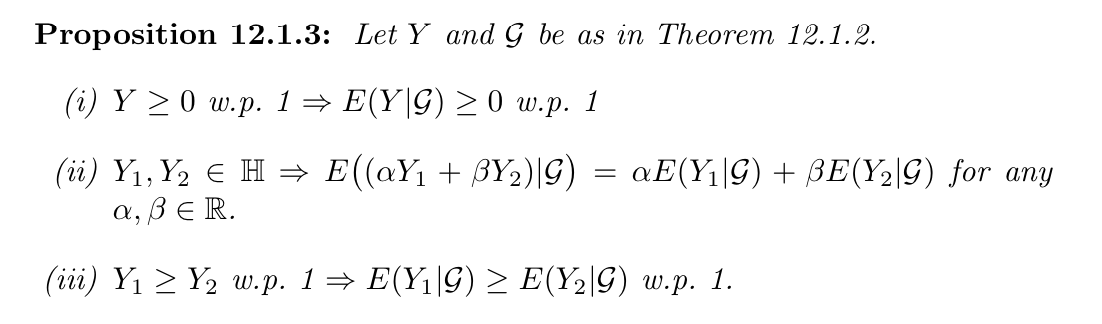

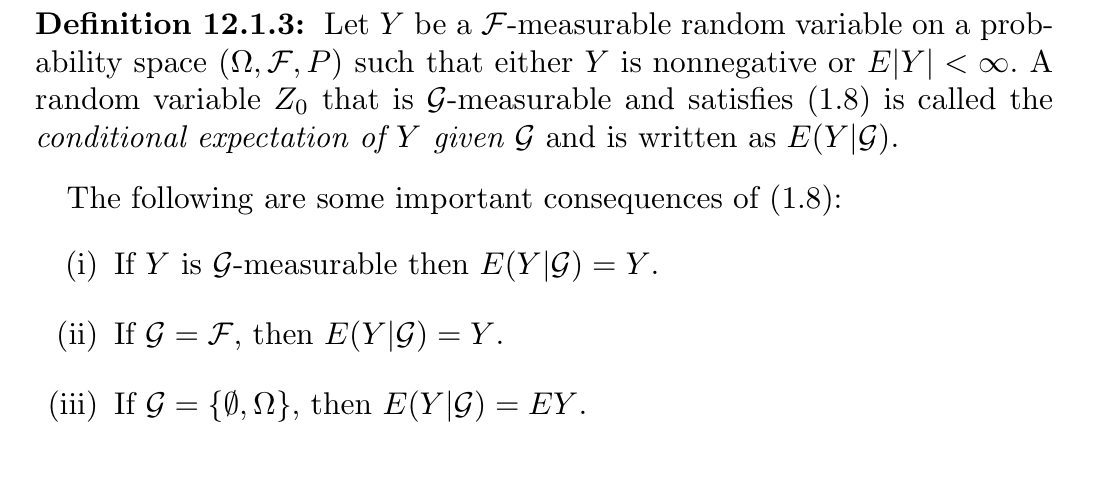

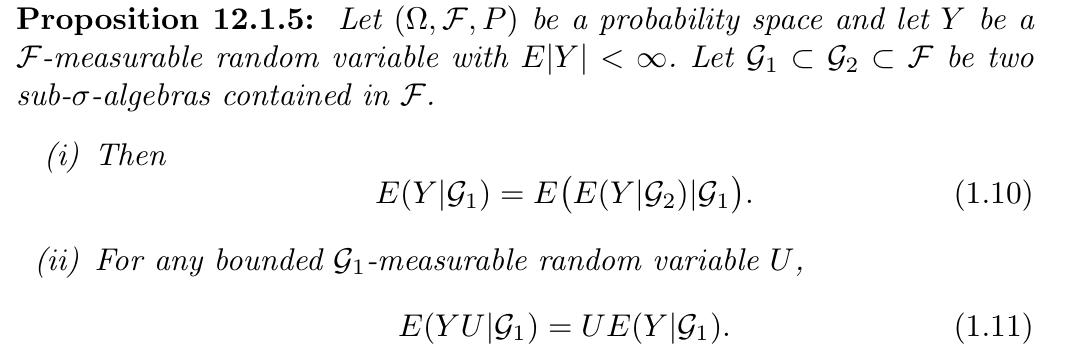

3.1.3.2. conditional expectation of Y given \(\mathscr{G}\)

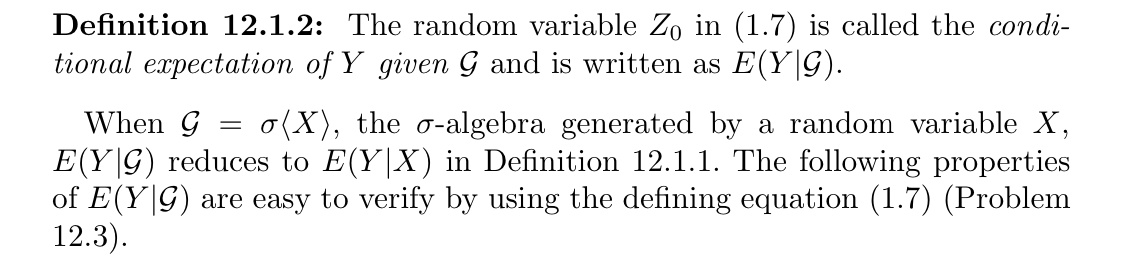

Def: conditional expectation of Y given \(\mathscr{G}\)

Usage: a more general situation

Note: other definition

Qua: => existence

Qua: => some qualities

Qua: => some more qualities (all expectation equation)

Qua: => the more general version of computation

3.2. special functions

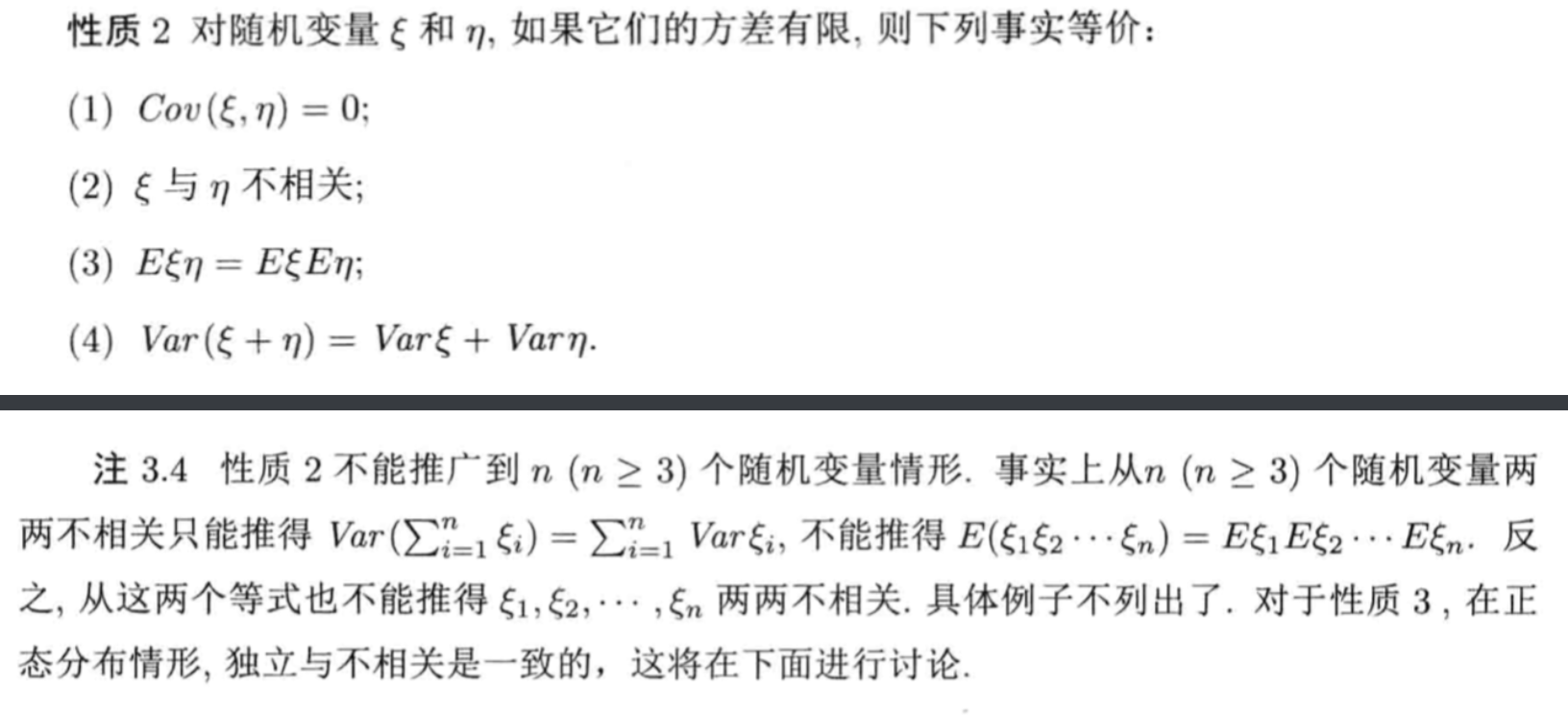

3.2.1. covariance

Def1.20: co-variance

s.t. abs < inf \[ Cov(X,Y)=E _{X,Y}(X-E(X))(Y-E(Y)) = number(X,Y) \]

- Qua1.21: => \(Cov(X,Y) = EXY -EXEY\)

- Qua1.22: => \(Cov(aX,bY)=abConv(X,Y)\)

- Qua1.23: => \(Cov( \sum_{n = 1}^{\infty}Xi,Y)= \sum_{n = 1}^{\infty}Cov(Xi,Y)\)

3.2.2. correlation coefficient

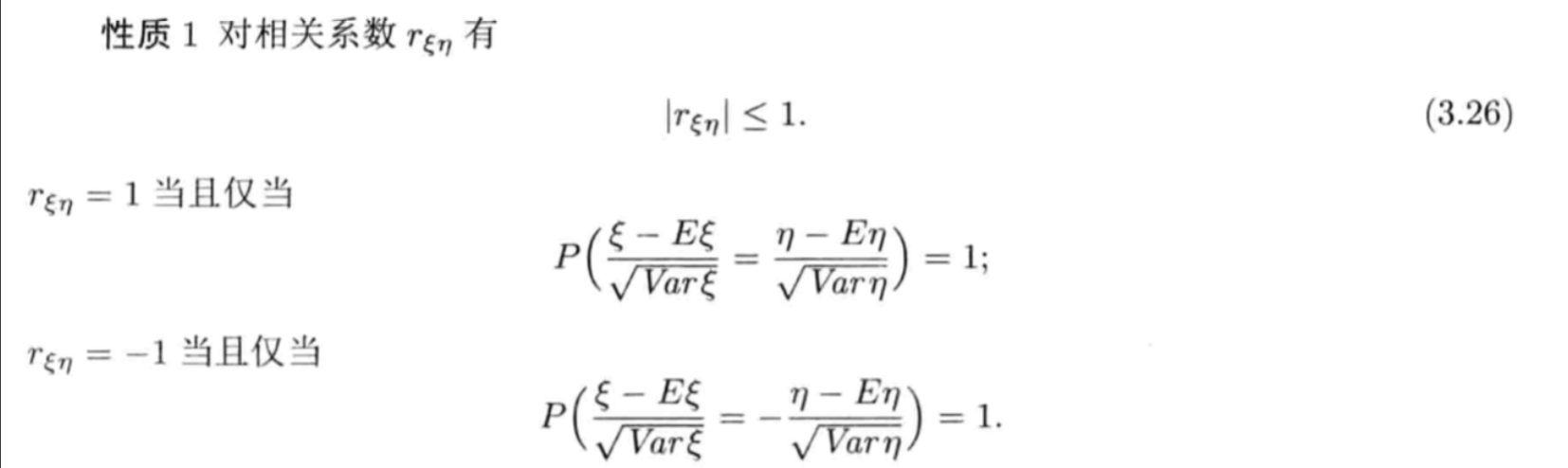

Def2.24: correlation coefficient

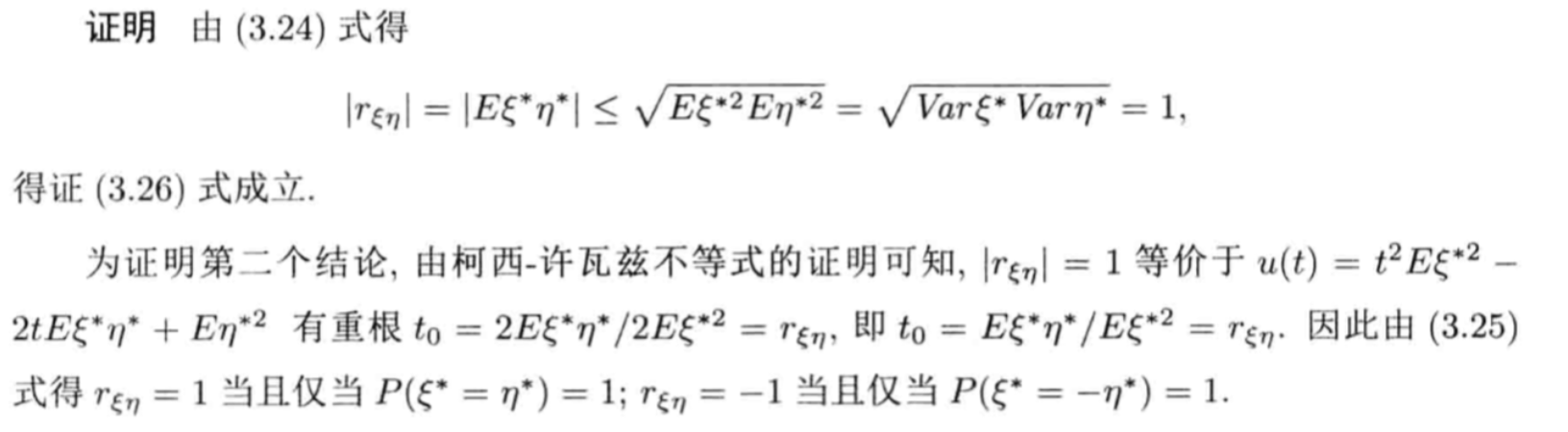

Qua2.25: => when r = 1 or -1

Proof:

Qua2.26: => relationship with E & Cov

3.2.3. conditional expectation

Def1.7: conditional expectation

$$ \begin{aligned} & E(X|H) = = _{x }x \ & E(X|H) =

\end{aligned} $$

\[ \begin{aligned} &E(X|Y=k)= \sum_{v}^{} v*p _{X|Y}(v|k)=number(k,X,Y) \\ & E(X|Y=k)= \int_{- \infty}^{\infty} v*p _{X|Y}(v|k)dv =number(k,X,Y)\\ & E(X|Y) = randomvariable(Y) \end{aligned} \]

Example:

Qua1.8: => total expectation fomula \[ E(E(X|Y)) = E(X)\\E _{Y}(E(X|Y)) = \sum_{k}^{}E(X|Y=k)P(Y=k)= E(X) \]

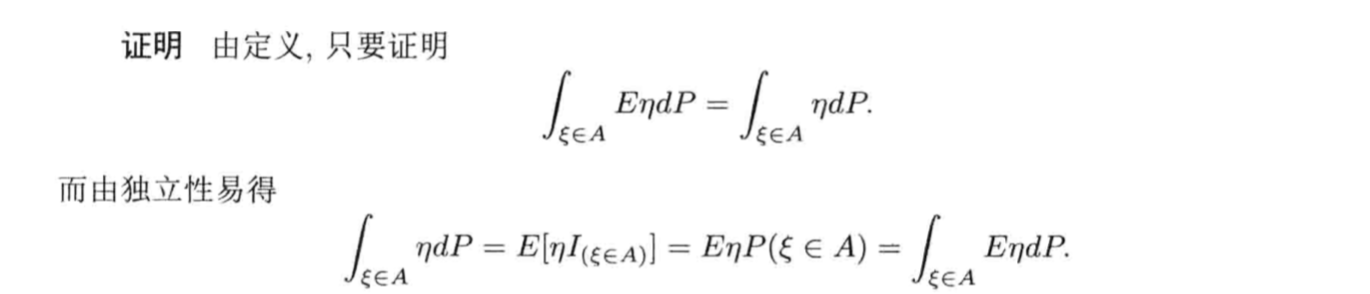

Qua1.9: => take out the known \[ E (g(X)Y|X)=g(X)E (Y|X) \]

Qua1.10: => Caughty \[ |E(XY|Z)| \leq \sqrt{E(X ^{2}|Z)} \sqrt{E(Y ^{2}|Z)} \\ |EXY|^{2} \leq E X ^{2} EY ^{2} \] Proof:

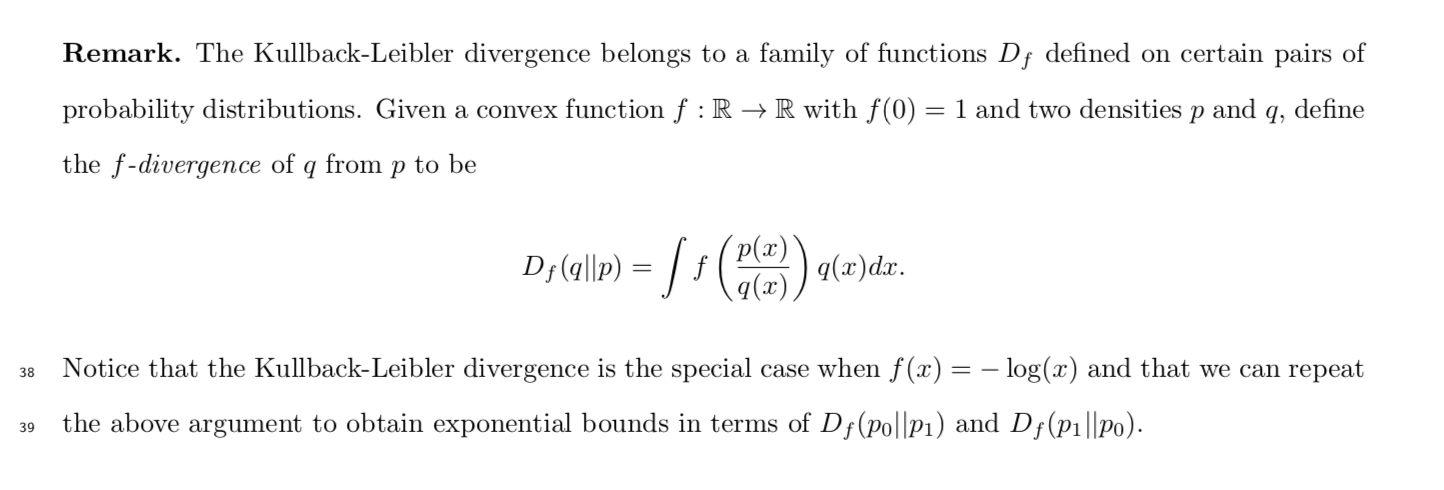

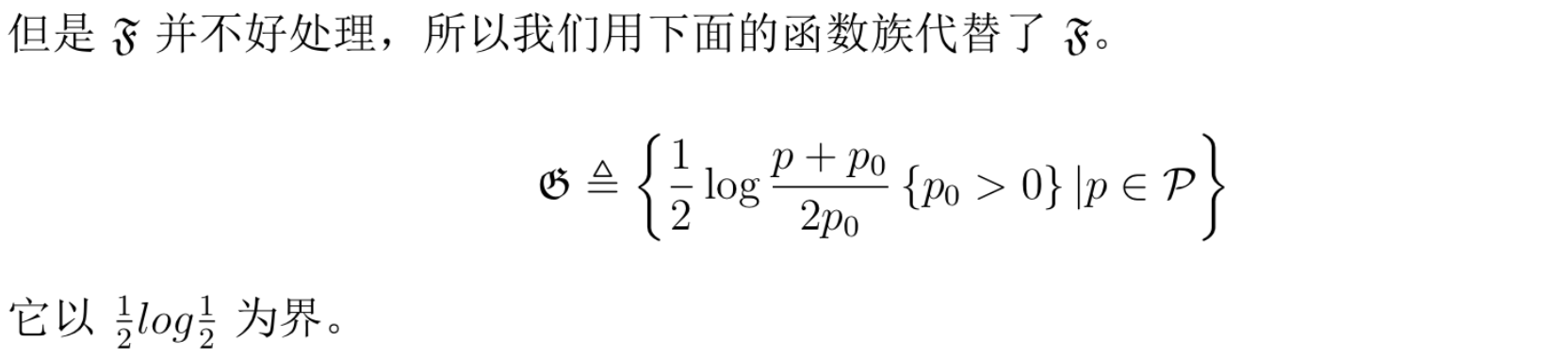

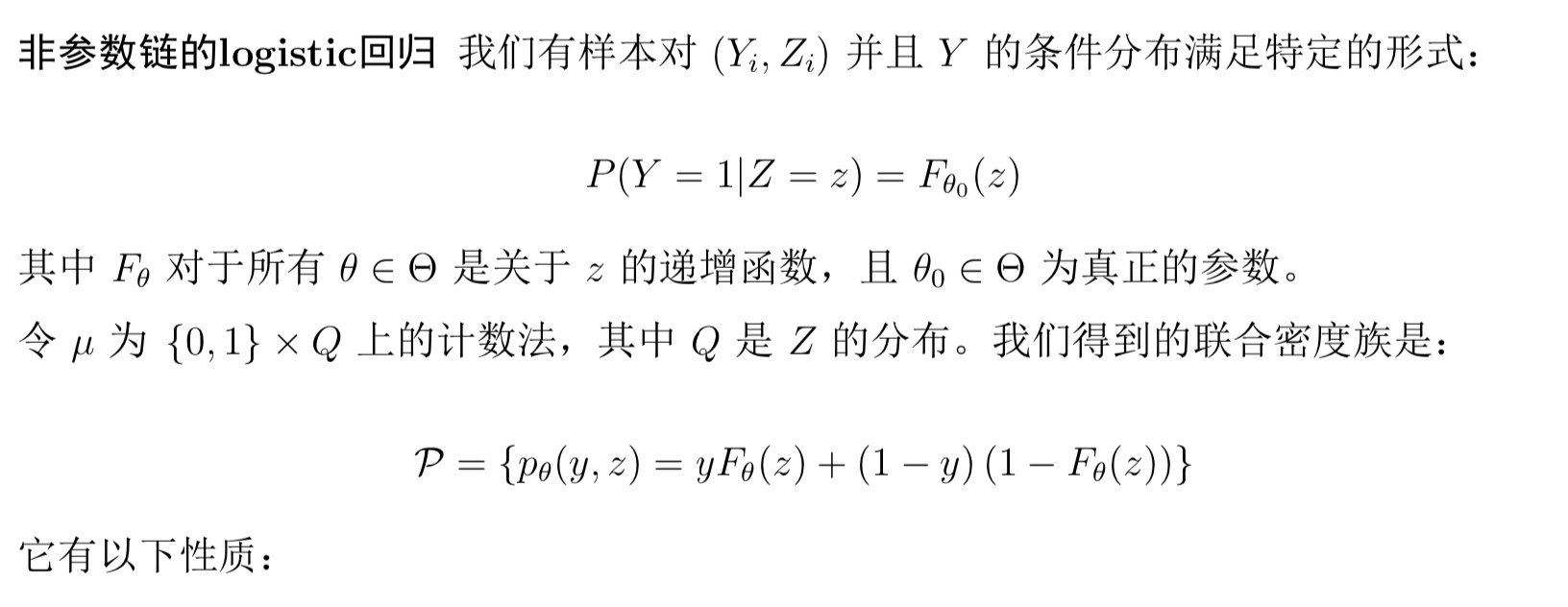

3.2.4. KL divergence (2-9)

Def: a group of function

Def:

Qua: accutually not a formal distance, but can be used to metric the distance between distributions.

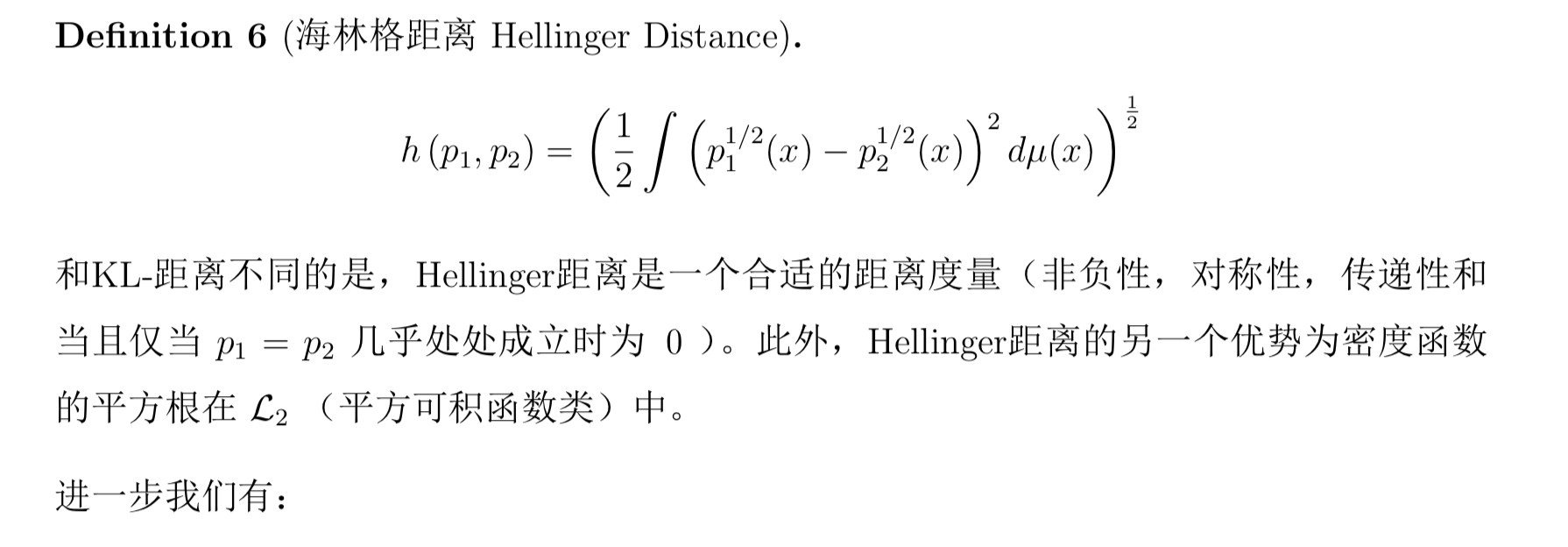

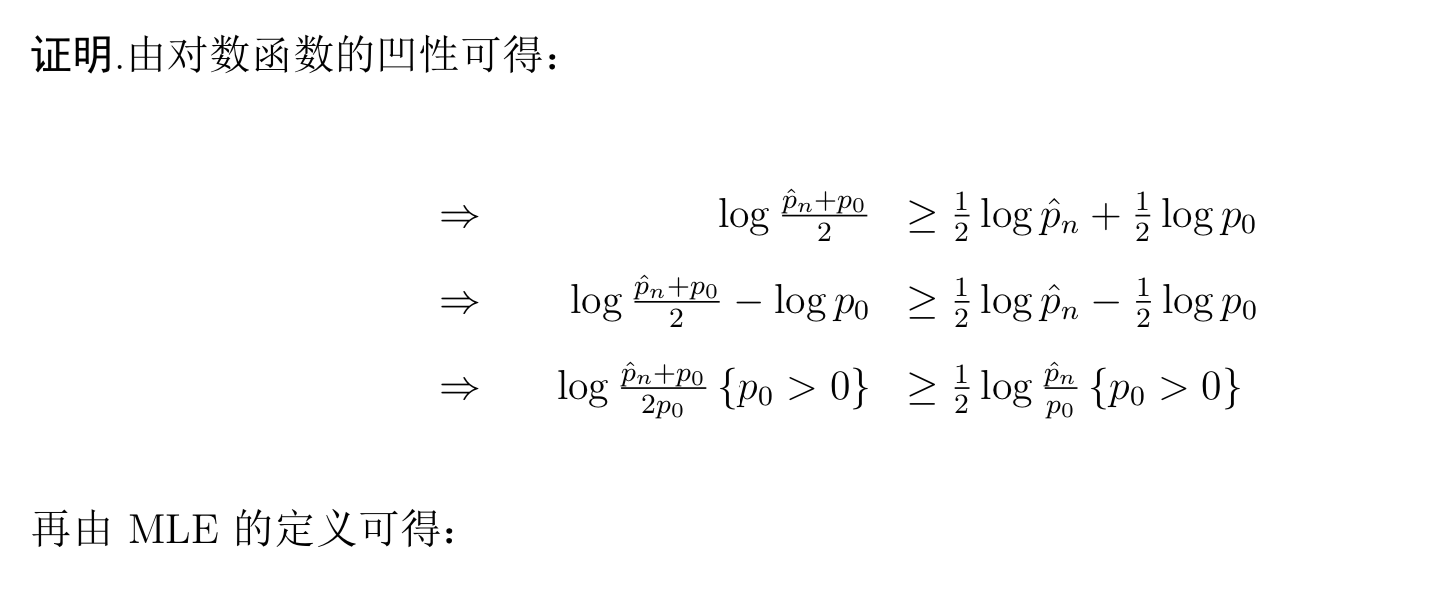

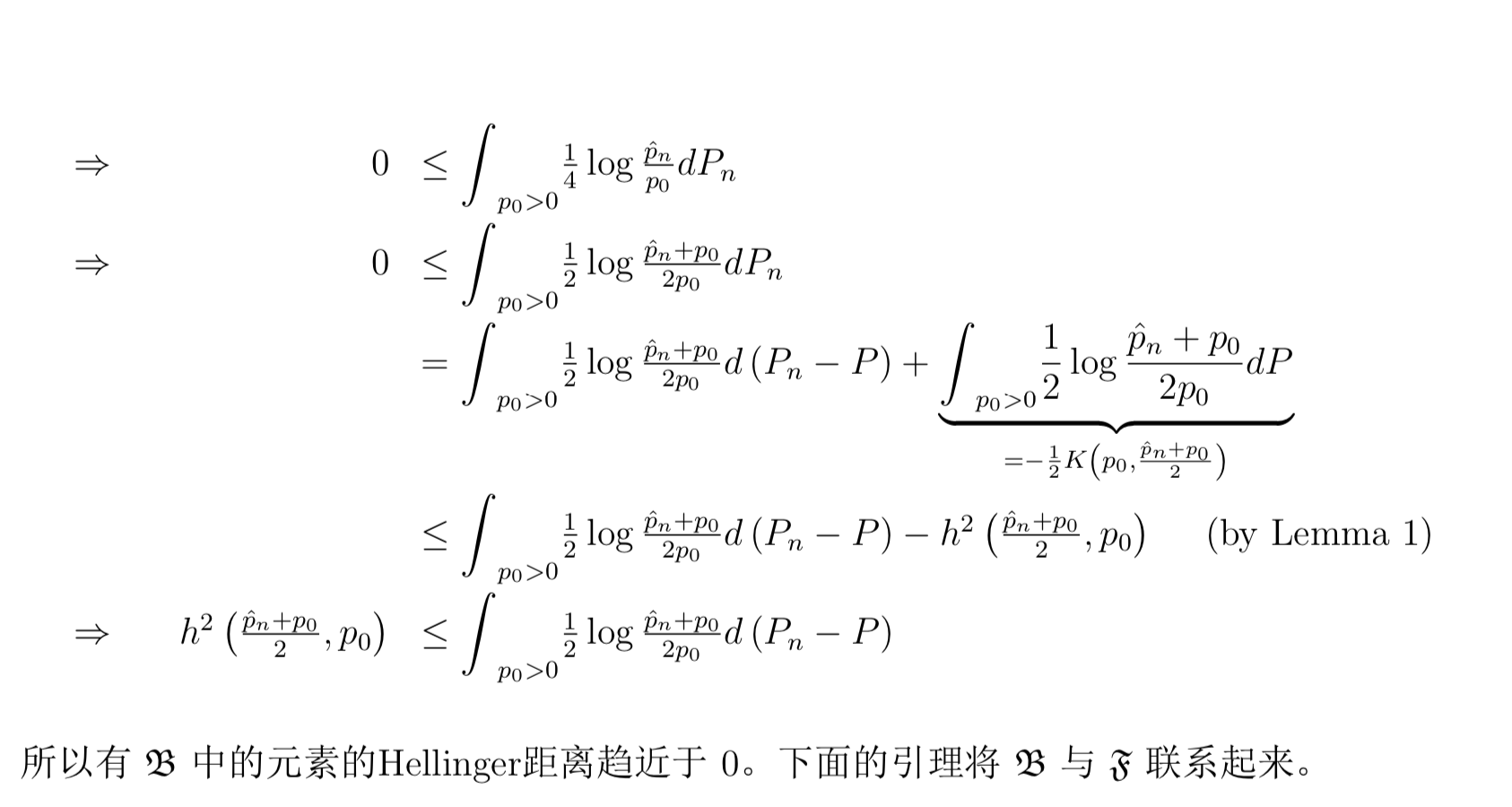

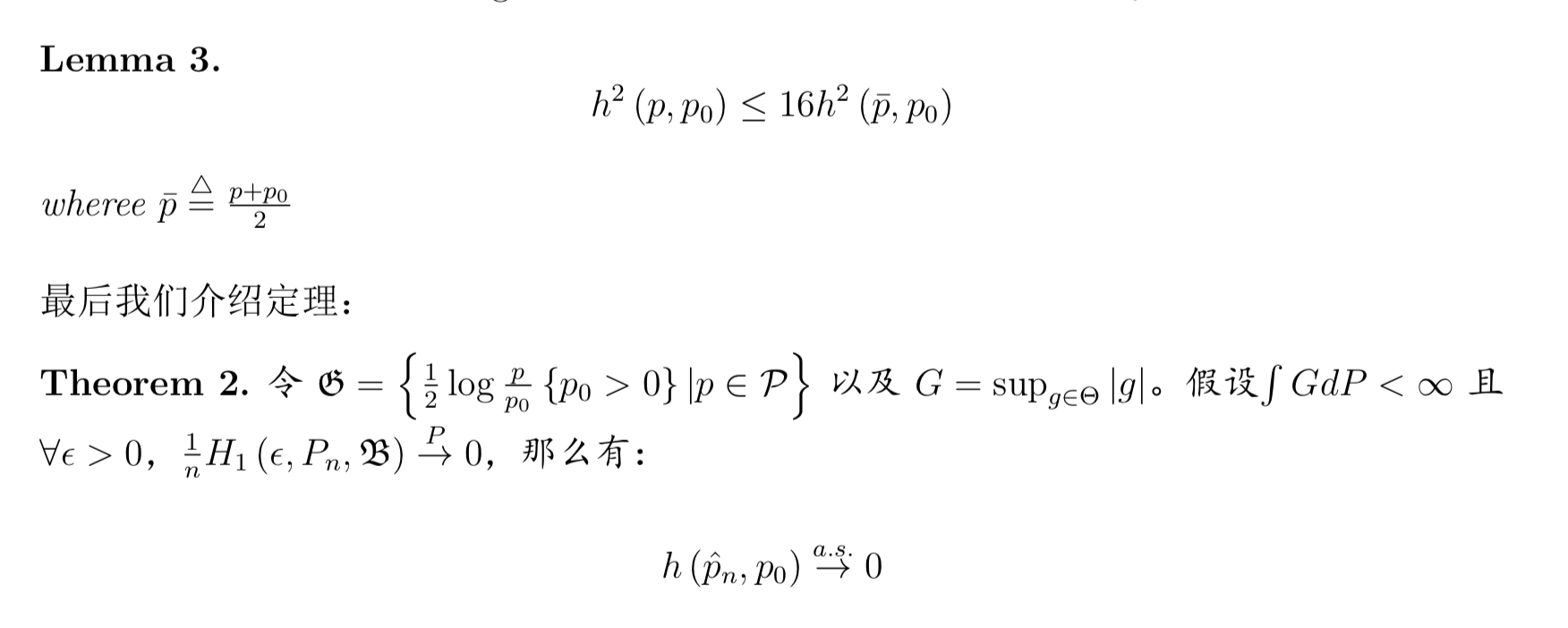

3.2.5. Hellinger distance (2-9)

Def: a group of function

- Def: Hellinger distance

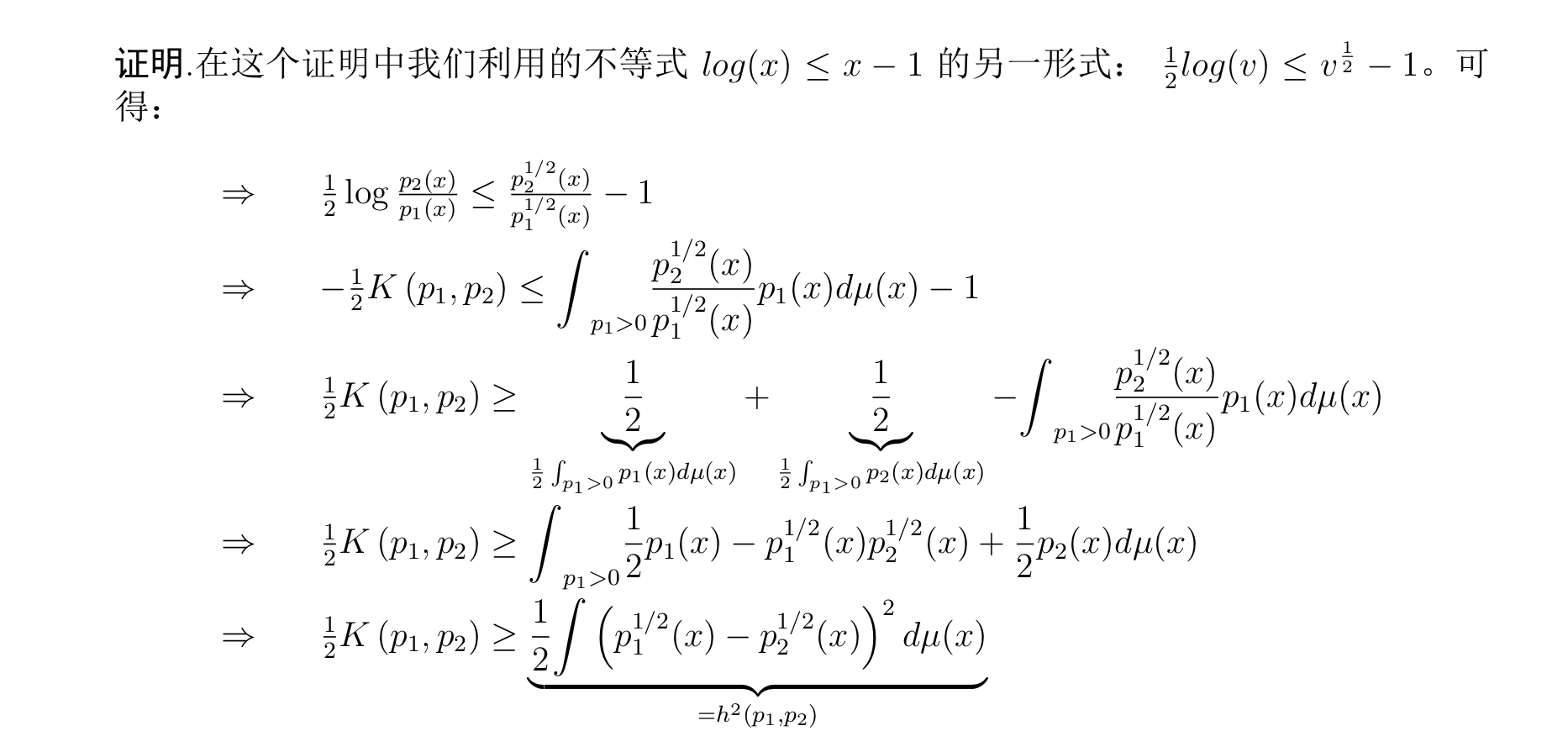

- Qua: => KL distance

proof:

Qua: => upper bound

proof:

acctually from MLE definition and KL and He relationship

acctually from MLE definition and KL and He relationship

Theorm: relation ship between above two group of function

- example:

t this distribution satisfy the Theorm, thus the empirical is very useful.

3.3. indepence & correlation

3.3.1. indepence

Def3.1: independence of random variable

\[ F_{XY} () =F _{X }()F _{Y}() \\p _{XY} = p _{X} p _{Y} \]

Qua3.1: Gaussian => ind

s.t. X1, X2 is variable gaussian \[ X1,X2 \text{ is uncorrelated = X1,X2 is independent} \]

Qua3.2: ind => E

s.t. X1, X2 independence \[ E(X1X2) = E(X1)E(X2) \]

Qua3.3: ind => uncorrelation

s.t. (1)X1, X2 independence

(2)X1 X2 var not inf \[ X1,X2 \text{ is uncorrelated} \]

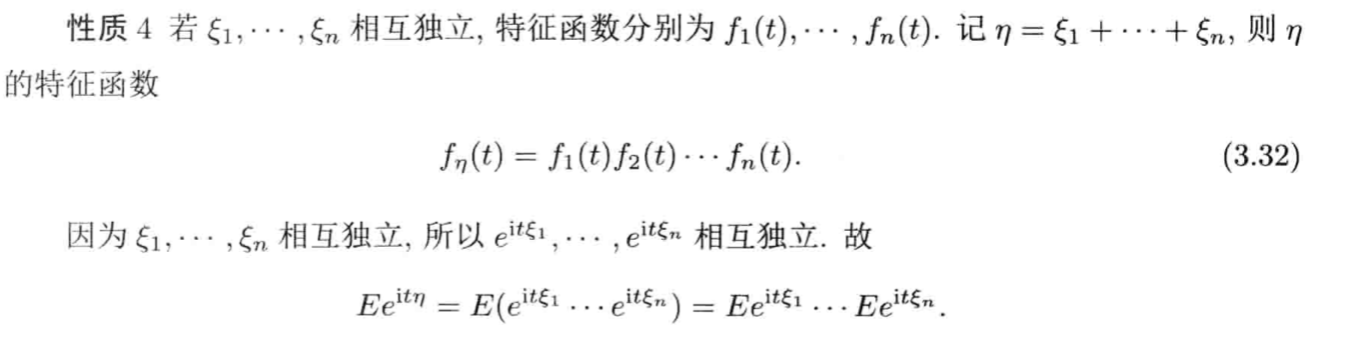

Qua3.5: ind => character function

Qua3.6: ind => conditional expectation

Proof:

3.3.2. correlation

- Def3.2: correlated \[ r _{XY} = \pm 1 \Rightarrow XY\text{ is probability 1 linear} \\ r _{XY} = 0 \Rightarrow XY \text{ is uncorrelated} \]

3.4. transformation

Theorm2.: transformation of continuous to continuous

s.t. (1) \(g(x)\) strictly mono

(2) \(g ^{-1}(y)\) has continuous derivation \[ (1) Y=g(X) \text{ is continuous random variable}\\ (2) g _{Y}(k) = \begin{cases} p(f ^{-1}(y))|f ^{-1}(y)'| & k \in f(x)值域\\ 0& otherwise \end{cases} \]

Theorm2.: transformation of continuous to continuous +

s.t. (1) \(g(x)\) strictly mono in non-overlap areas. And areas add up to \(\infty\)

(2) $ g ^{-1}(y)$ has continuous derivation in non-overlap areas. \[ same \]

Therom: transformation of continuous vector(x1,x2..xn is continuous) to continuous \[ (1) Y=f(x1,x2,...,xn)\\ (2)F _{Y}(k) = \int \limits_{Y \leq k}p_{X1...Xn}(x1,...xn)dx1...dxn \]

Theorm: transformation of continuous vector(x1,x2..xn is continuous) to continuos vector

s.t. (1) m = n

(2) ... \[ ... \]

Theorm2.1x**: convolution equation \[ P(X+Y=c) = \sum_{k = 0}^{r}P(X=k)P(Y=c-k)\\ P_{X+Y}(c) = \int_{- \infty}^{\infty}p _{X}(k)p _{Y}(c-k)dk \\ \]

3.5. classic bounds

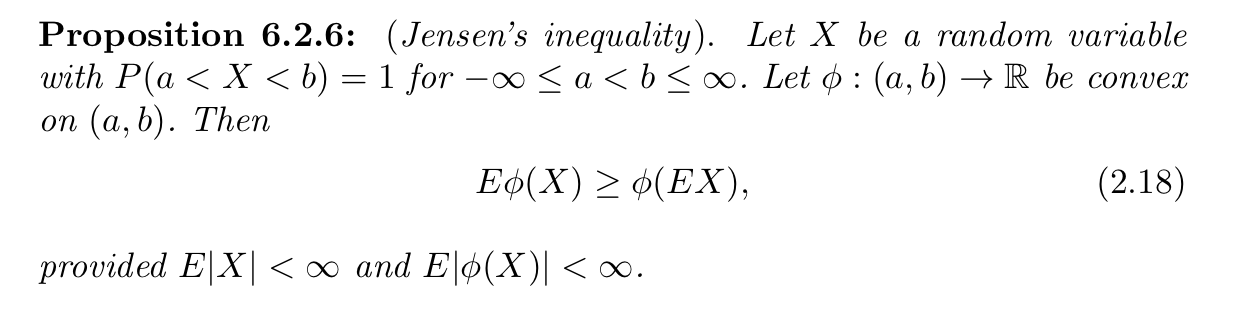

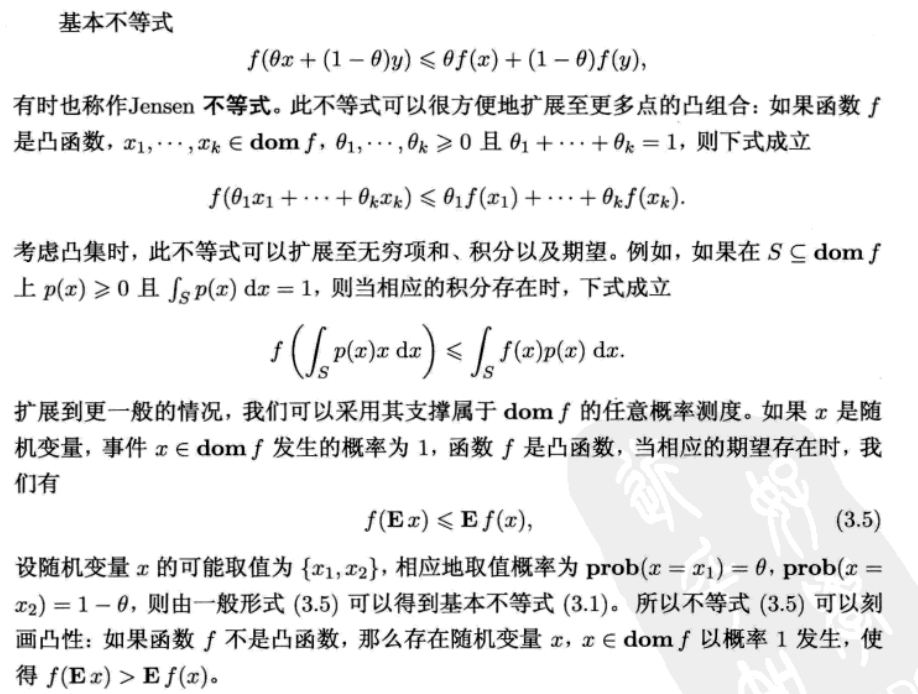

3.5.1. jensen inequality

Def:

another

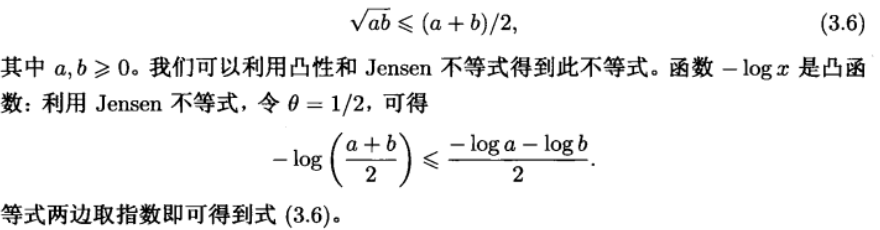

3.5.1.1. geometric inequality

Def:

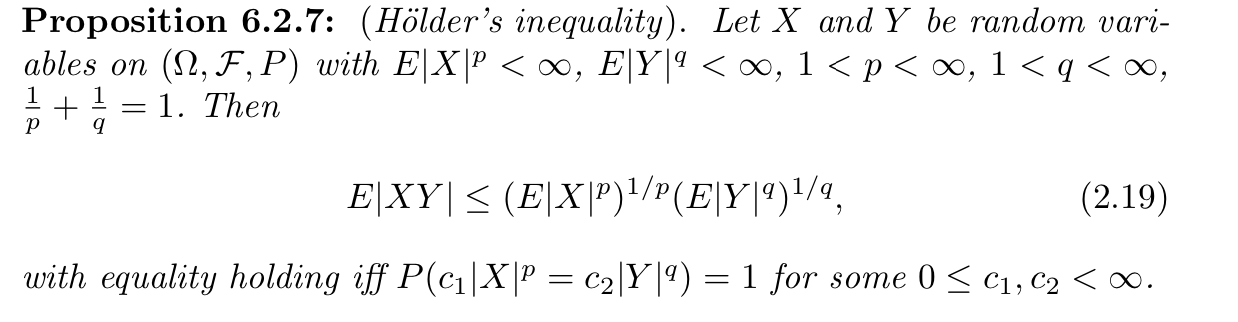

3.5.1.2. Holder's inequality

Def:

Note:

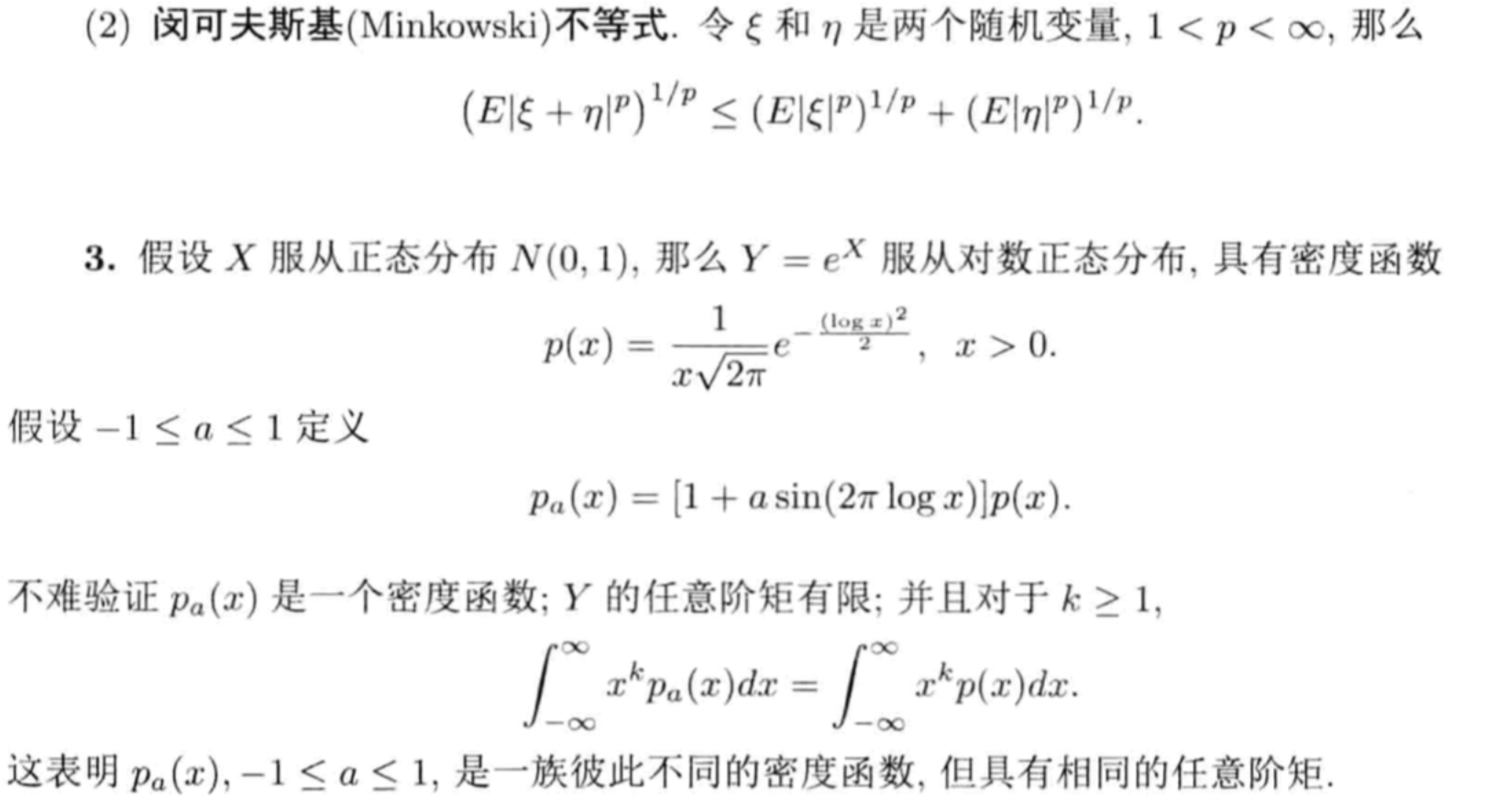

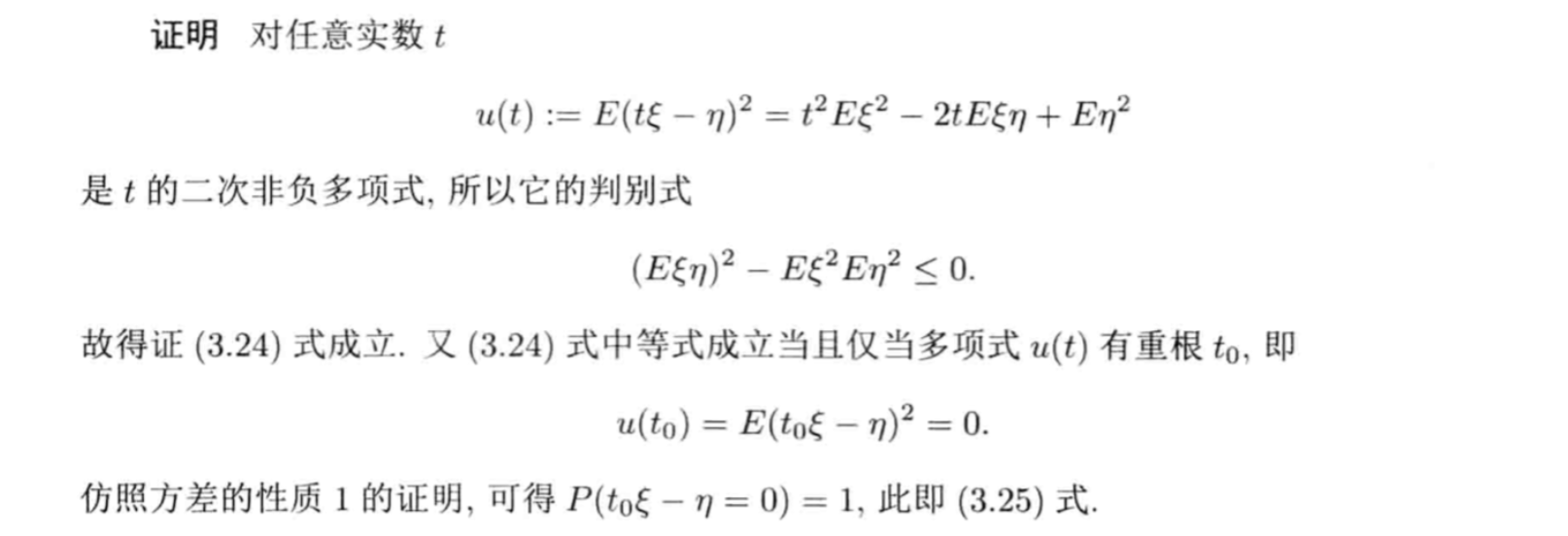

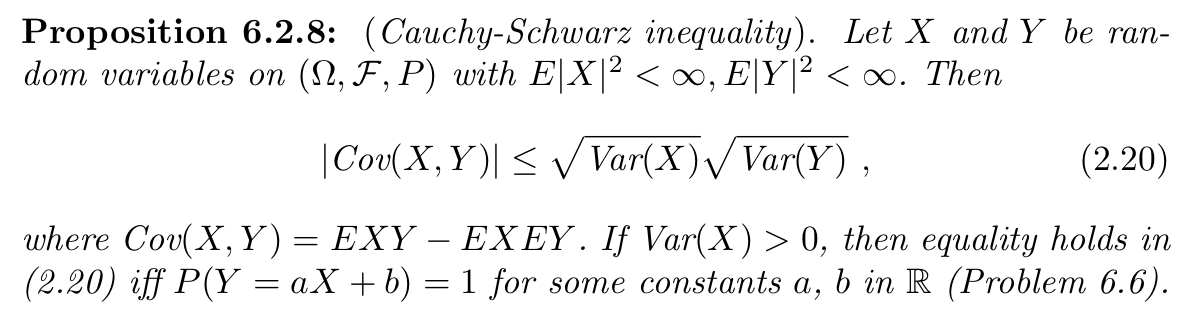

3.5.2. Cauchy-Schwarz inequality

Def:

3.5.3. Minkowski's inequality

Def:

3.5.4. markov bound

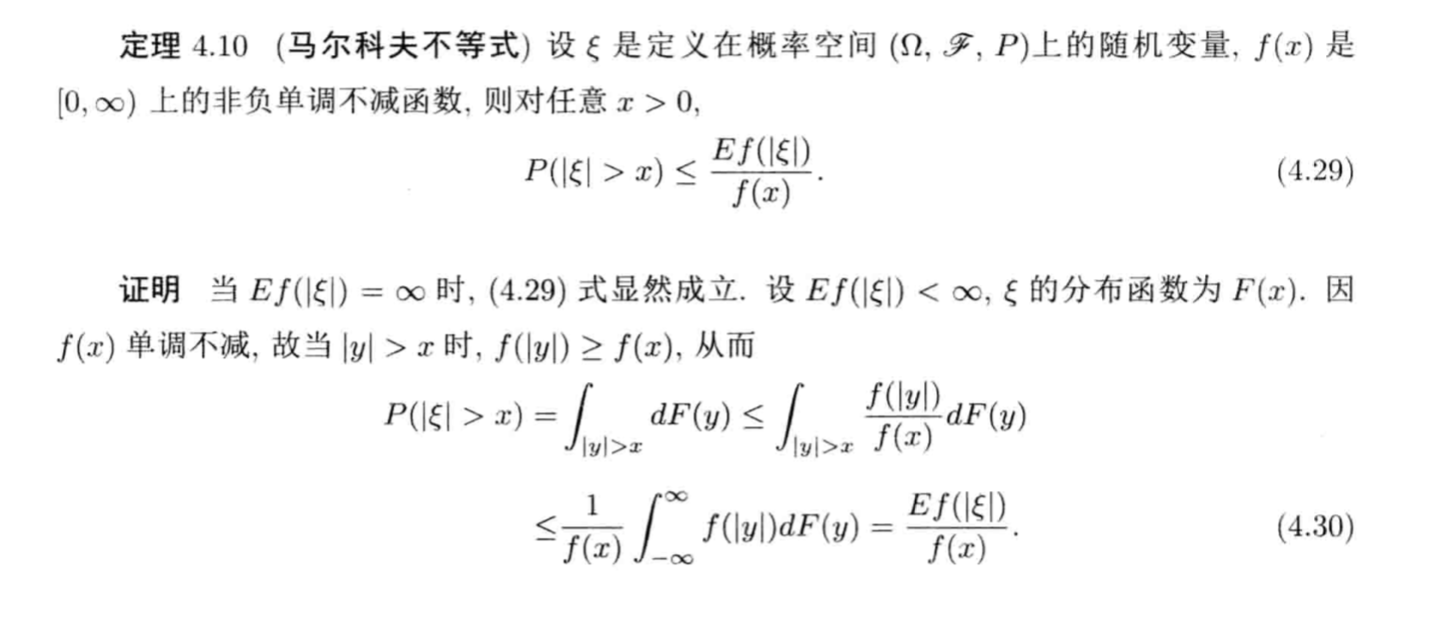

Theorm: markov bound

Usage: measure the prob that of deviation will larger than e

s.t. V(X) \[ P(|X-E(X)| \geq e) \leq \frac{V(X)}{e ^{2}} \]

1-14

Example: that markov's only a very weak bound (1-14)

3.5.5. chebshev bound

Corollary : => chebshev bound

1-14

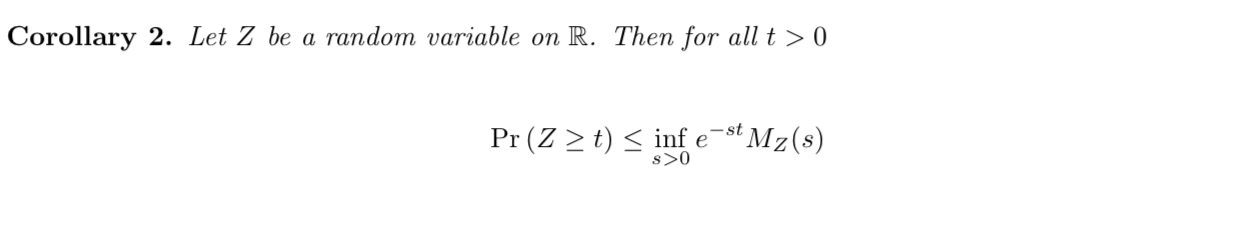

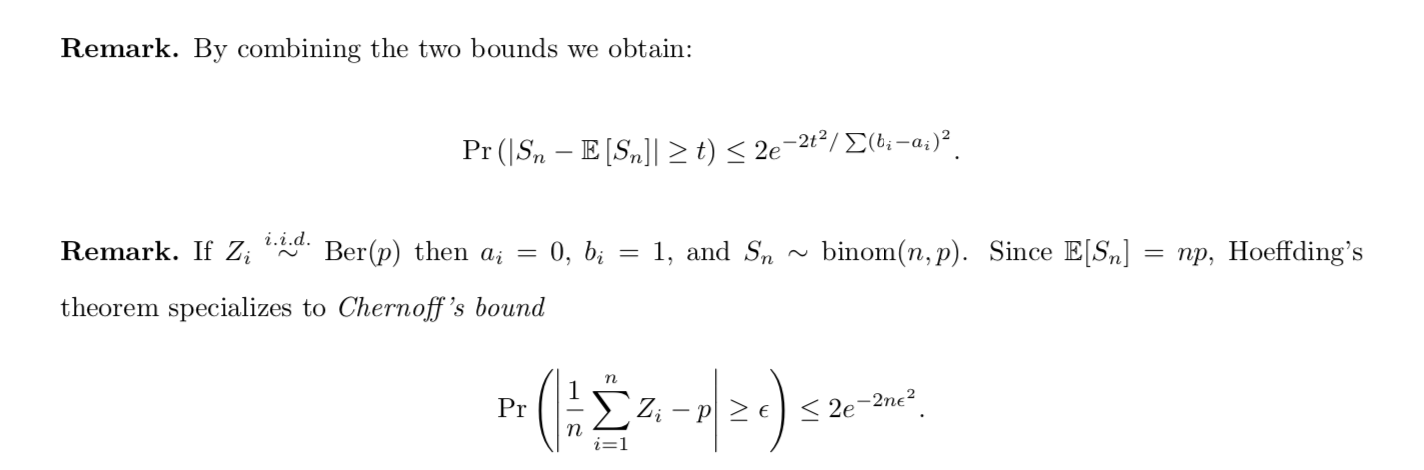

3.5.6. chernoff bound

Corollary: => chernoff bound

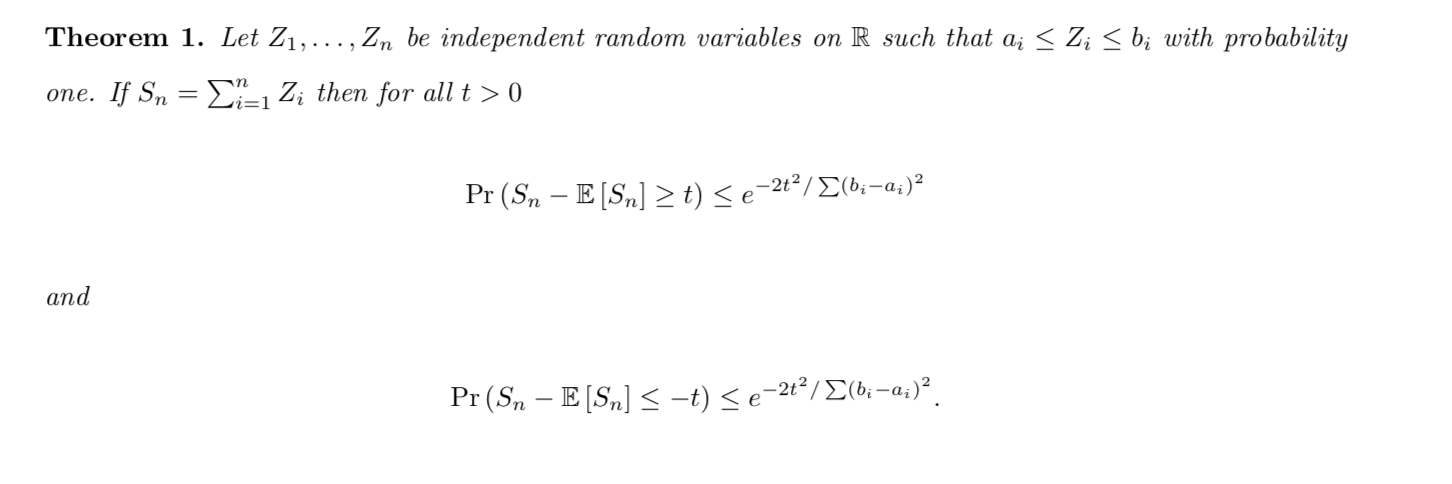

3.5.7. hoeffding bound

3.5.7.1. heffding bound

Intro: insights of hoeffding bound

Lemma: => bounds (used to prove hoeffding) (1-14)

Proof:

Theorm:: => hoeffding's inequality (1-14)

(2-5)

Proof:

Example:

Corollary: => more bounds

3.5.7.2. bound differences in equlity (1-15, 1-16)

Theorem: bound differences inequality (1-15)

Usage: adding a mapping on hoeffding bound

(1-16)

Proof:

Example: (1-16)

Example 2 : (1-16)

Usage: in this example we use sup(Eg-E^g) as a random variable.

Example 3 : (1-16) the loss function

3.6. limit theory

Def: tight & uniformly tight

Qua: suff & neck

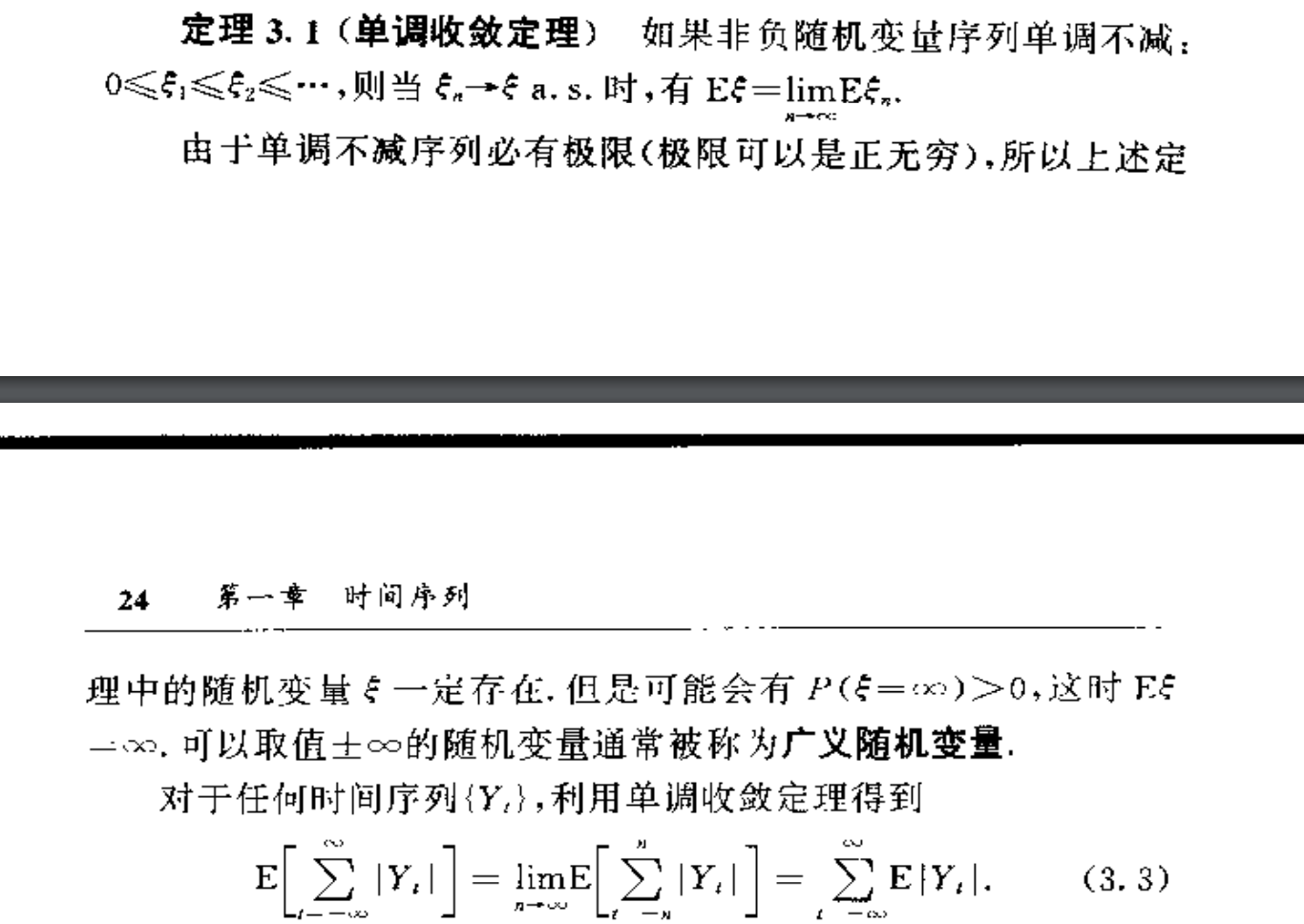

Theorm:: mono limit

Theorm: control limit

Theorm: different converges

Theorm: BC(3-6)

3.6.1. converges in distribution

Def: convergence in d

(2-1)

(2-10)

(2-10)

(book)

Note:

Qua: suff & necc

(2-1)

(2-1)

Qua: pn converge =>

Qua: operation

(book)

(2-1)

(2-1)

(2-2)

3.6.1.1. Helly theorem

Theorm: Helly, existence (book)

Proof: long

Theorm: Helly2, whether function still converge (book)

3.6.1.2. Levy theorem

Theorm: Levy, converge and cf (book)

Usage: special function & density one on one

Theorm: Levy backwards (book)

3.6.1.3. centrol limit theorem

Def: centrol limit theorem (sum of x --d--> gaussian) (book)

Theorm: sum of iid gaussain --d--> gaussian (book)

Note :

Theorm: sum of iid --d--> Gaussian (book)

Proof:

Theorm: sum of independent --d--> Gaussian (less strict condition) (book)

Theorm: sum of independent --d--> gaussian (less strict condition) (book)

3.6.2. converges in probabilty

Def: converges in probability

(2-1)

(3-6)

(book)

Note: why distribution not enough so include probability is nemeses

Qua: necc & suff (book)

Qua: E(zn-z) =>

(3-6)

Proof: markov inequality

Qua: => d

(2-1)

(book)

Qua: operation

(2-1)

(2-2)

(book)

3.6.2.1. tight variables

Def: tight variables (2-1)

3.6.2.2. oh-pee

Def: Op,op (2-1)

Qua: operation

3.6.2.3. weak law of large numbers

Def; law of large numbers (book)

Theorm: sum of iid Bernoulli --p--> E (book)

(2-2)

Theorm: sum --p--> E (less strict)

Proof:

Theorm: sum of invariant --p--> number (less strict ) (book)

Theorm: sum of iid --p--> number( more strict )(book)

3.6.3. converges in probabilty 1 / almost

Def:converge in probability.1

(2-1)

(3-6)

(book)

Note:

Qua: necc & suff (book)

Qua: P => (3-6)

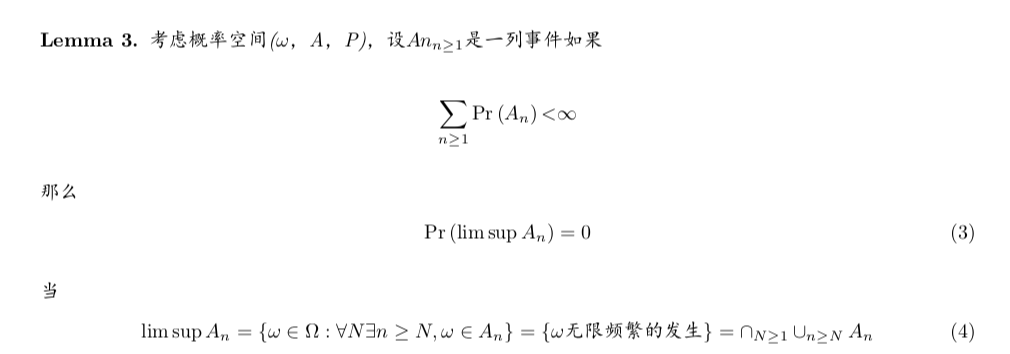

Proof: from Borel-Cantelli Lemma

Qua:P(a-b) => (book)

Qua: => P (2-1)

Qua: => lim(E|Xn-X|) (2-1)

Qua: => lowerbound(lim inf E|Xn|) (2-2)

Qua: => lim(E|Xn|) (2-2)

Qua =>lim(EXn) (2-2)

Qua: operation (2-1)

3.6.3.1. strong law of large numbers

Def: strong law of large numebrs (book)

Theorm:sum of bernolli --as--> number (book)

Proof: too long

Therom : sum of iid --as--> E. (book)

(2-2)

3.6.3.2. uniform law of large numbers

Def: sum of f(bernoll) --as--> number

3.6.4. convergence in r th mean

Def: converge in rth means

(2-1)

(book)

Qua: => p

3.6.5. continuous mapping theorem

Since weak convergence does not hold for all probability measures, we need conditions on the set C on which

the limiting random element concentrates.

Def: < (web)

Def: separable & regular

(2-10)

(web)

Theorem: continuous mapping theorem

(2-10)

(web)

Theorem: stochastic equicontinuity

(2-10)

(web)

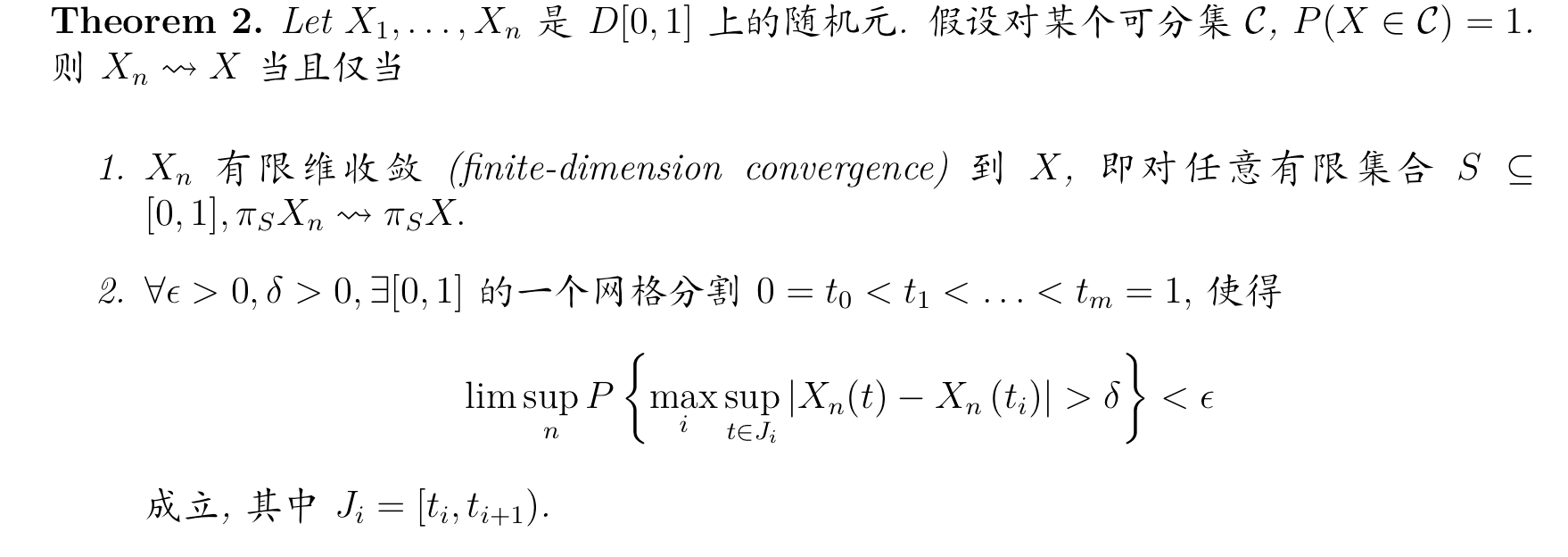

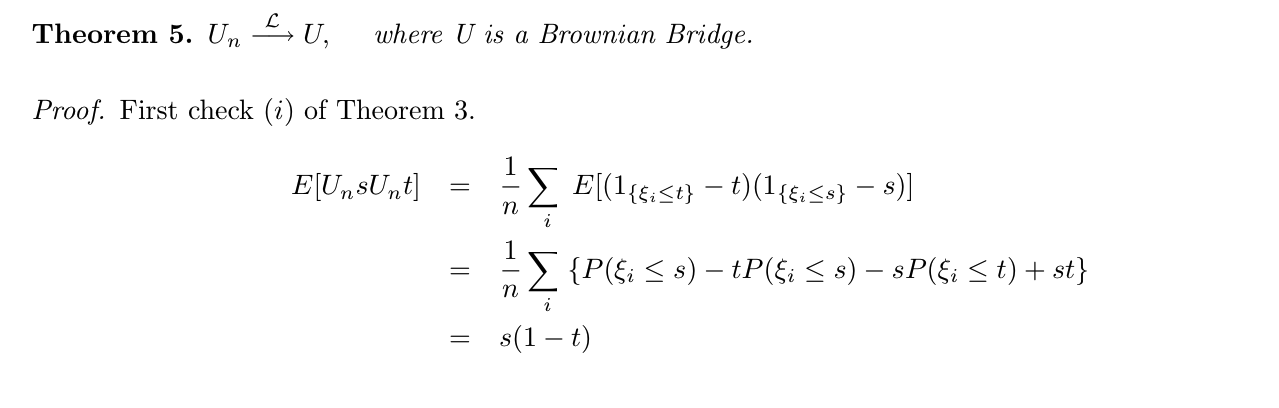

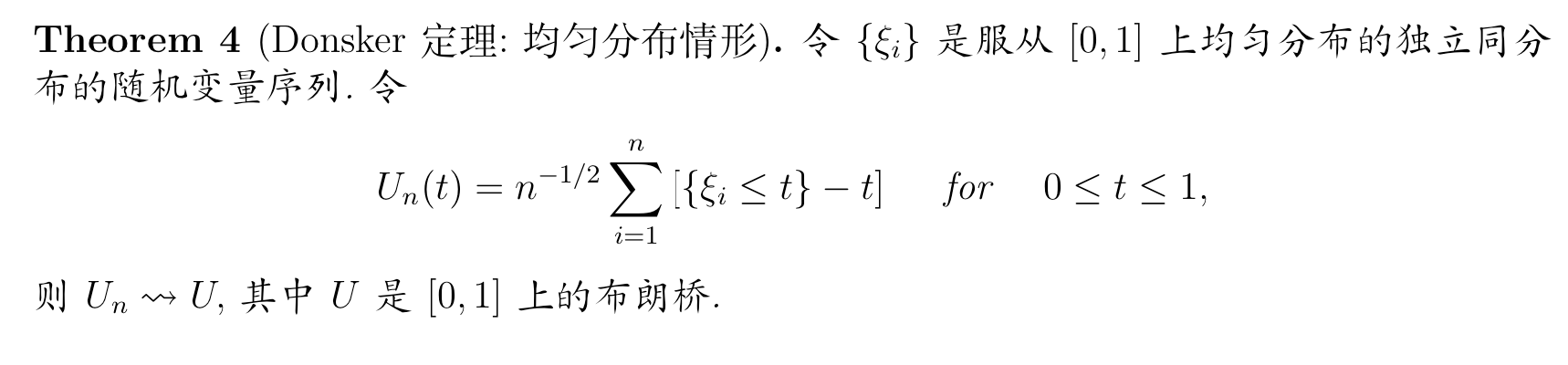

3.6.6. Donsker's Theorem(2-10,11)

Intro: why we need donsker's theorem (2-10)

Theorem:Donsker's Theorem v1(2-10)

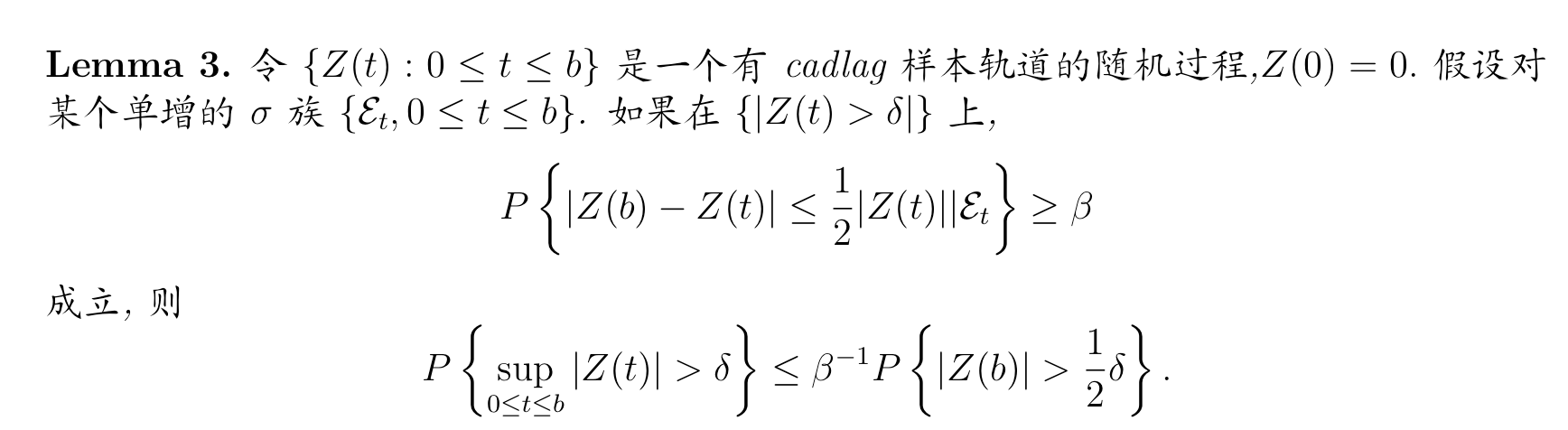

Lemma: (web)

Theorem: Donsker's Theorem v2(2-11)

Proof: see archive

Theorem: Donsker's Theorem v3(2-11)

Proof: see archive

4. random vector

4.1. distribution

4.1.1. joint pdf

Def: joint pdf

4.1.2. margin pdf

Def:

4.2. special functions

4.2.1. expectation

Def: E

- Qua: => basic

- Qua: => basic

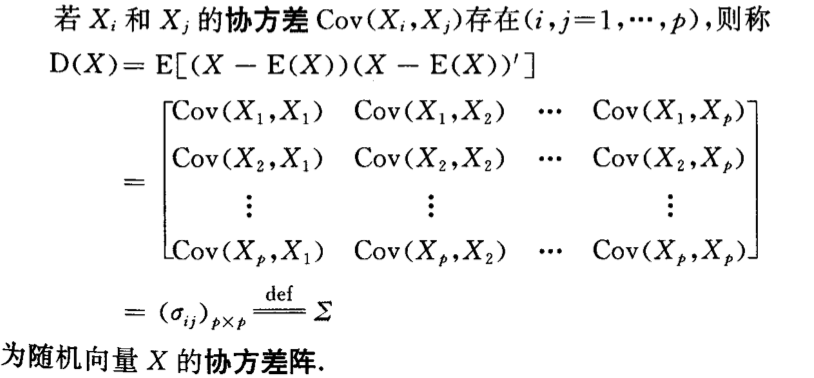

4.2.2. covariance matrix

Def: covariance of X

Qua: => non-negative

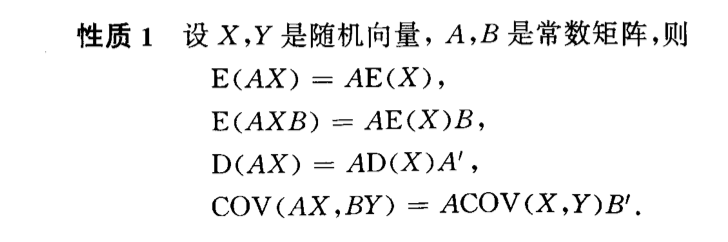

5. relationship between vectors

5.1. special functions

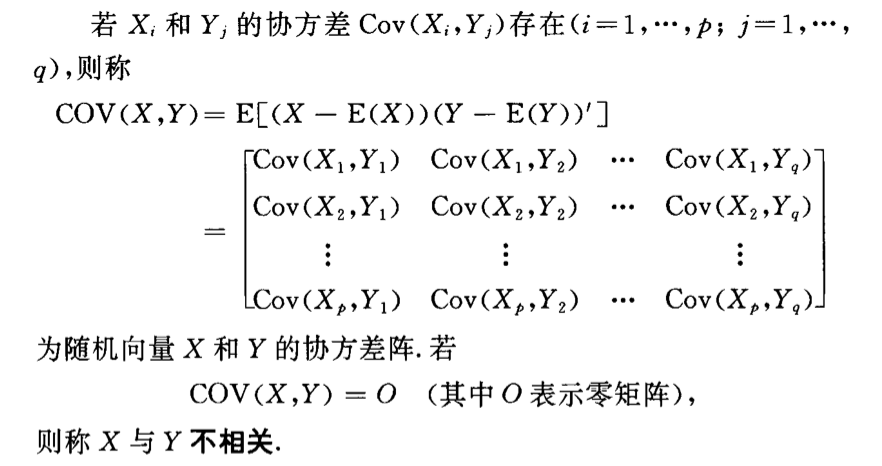

5.1.1. covariance matrix

Def: covariance

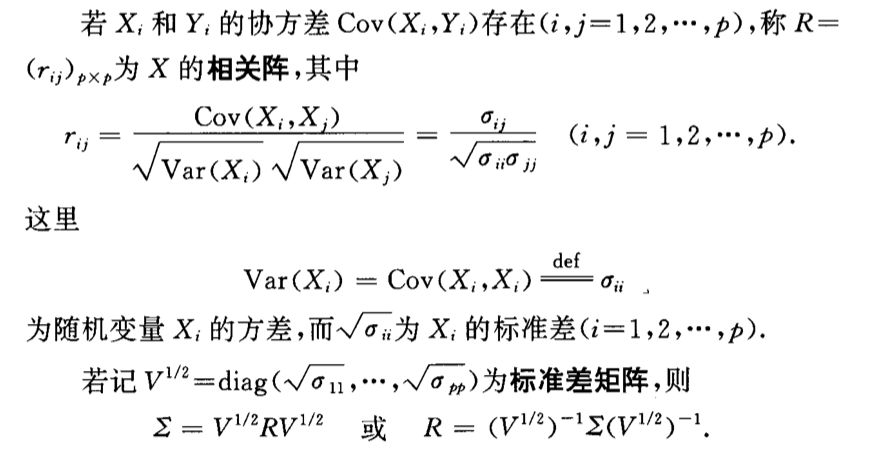

5.1.2. coefficient matrix

Def: coefficient matrix

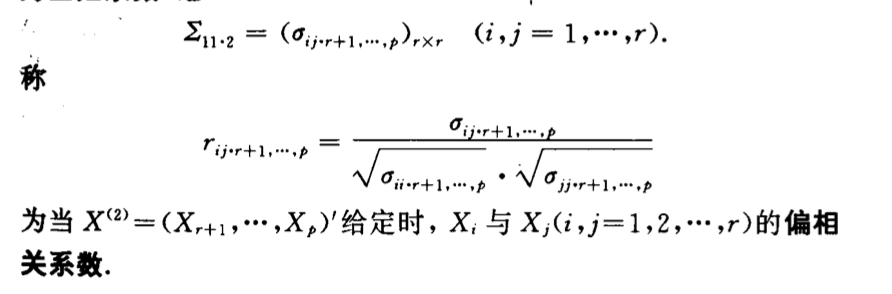

5.1.3. correlation coefficient

Def: correlation coefficient

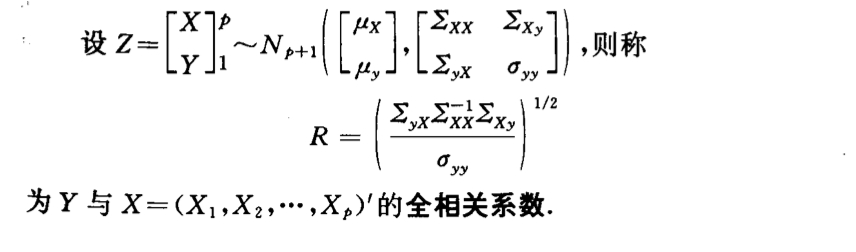

Def: skewed correlation coefficient

5.2. independence & correlation

5.2.1. conditional of itself

5.2.1.1. conditional pdf

Def: conditional pdf

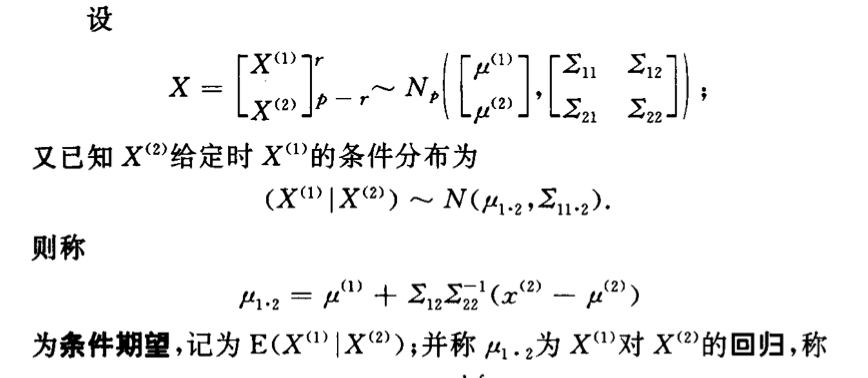

5.2.1.2. conditional expectation

Def: con-E

5.2.2. independence

- Def: independence

- Qua: => COV = 0

5.2.3. correlation

Def: correlation